The effects of capitalism result from its logic of infinite growth for the value created, taking the production of useful goods and services for Humanity as a subsequent and not the central objective. At the top of the decisions are intelligent evildoers and ambitious imbeciles whose only aim is to create value, in the case of so-called entrepreneurs or, to raise GDP in the case of political classes.

Summary

1 – The affirmation of a Big Brother

2 – Total credit directed to the non-financial sector (% of GDP)

3 – Total credit granted to the public sector (% of GDP)

******* // \\ *******

1 – The affirmation of a Big Brother

The financial system as the dominant element in contemporary capitalism, takes advantage of the immaterial nature of the information it uses and compiles, publishes with great today, without going into great detail as to their dependents atomized – businesses, particularly small and medium-sized and , families, individuals. It is the BIS – Bank of International Settlements that is in charge of this aggregating function, by countries and groups of countries, such as the Euro Zone or the G20.

Obviously, on a global scale, even though it is composed of several great powers, some more autonomous than others, installed in midst of great rivalries, these powers are nonetheless competing, fighting, concerting, within the scope of variable geographies of power.

The volatility of financial markets intersects with the speed with which transactions are made; the global character of his work makes him knowledgeable about heritage, income, transactions and consumption, the place of work and housing, travel and, travel, in a degree of detail beyond what we can imagine. On the other hand, the promiscuous connection with the state apparatus allows the financial system and the state powers to have a fine knowledge of our lives.

Quantum computing will allow, with big cost savings, storage, treatment and, the exchange of data, with unprecedented amounts of information, in a very short time and at very low cost. And it will join another great leap forward, the abolition of physical cash (possibly in 2023, the Eurozone).

Money, in its many forms of physical presentation, is something that has existed, in various forms, since the most ancient antiquity, to facilitate exchanges; its abolition is unprecedented denudation on the part of States, the financial system, technological giants specialized in collecting detailed information about people (Google, Facebook …) and Big Data. The plan that Google intends to execute in NewYork, in harmony with Andrew Cuomo, is configured with digitalization, teleworking, atomization, impoverishment, absence of rights; all properly monitored, either in spending, both in taste, contacts and, exchanges of information, a plan recently well explained by Naomi Klein .

In capitalism, money is the blood that circulates in its veins – in natura (currency and notes) or under a virtual way as deposits, stocks, bonds and these virtual elements called derivatives. In the next future, all records of income, acquisitions, donations, all transactions in which we participate, go through a crucible called the financial system. This, in turn, closely related with the States and, monitoring the political classes, will facilitate the addition of the fiscal drain on the job, such as pay as premium, for state intervention in the pacification of the common people, in the work; or, the dismantling of any contestation, with an efficiency far superior to the performance of political oppositions, today, to a large extent, mere folklore. As for personal data, its degree of updating, in real and historical terms, will be used, indistinctly by the financial system and by the state entities themselves, which,today, in many cases, spend resources on databases, which are too often poorly constructed and outdated.

In the case of Europe, there will probably not be a full replacement of the known physical currency, recognizable Christine Lagarde , president of the ECB. In July of the current year, the Bank of France chose, among other candidates, Accenture, HSBC (an acronym for Hong Kong and Shanghai Banking Corporation) and, one of the main banks in the world and also Societé Generale for an experience of using the digital euro. This apparent Bank of France leadership materialized shortly before in a positive test of a digital euro on a blockchain . It is known that post-Brexit Britain is also studying the digitization of the currency and that the Italian Banking Association intends to accept the digital euro .

Another step in the transition to reality as imagined by Orwell several decades ago, inspired an exquisite democrat called Stalin, the great architect of state capitalism which, respectfully, developed the thesis of Lenin, admirer of Taylorism and Fordism, “scientific” ways of organizing work, increasing productivity and the share of value available to capitalists. In capitalism, the more concentrated and totalitarian power is, the more the abstract role of work is reaffirmed, only as it generates pain of value, regardless of whether the product is a shirt, a television or, a war airplane. The production of goods or services aims at reproducing the invested capital while the goods produced are just means for that purpose. Its usefulness to people is not central, it is ancillary,it follows the need for capital for its accumulation to infinity. And if the planet is insufficient to contain the capital’s gluttony … so much the worse for the planet.

Today, the political and economic dominant force, it is not a nation-state with guarded borders and police on every corner or, huge holder of military power; it is a composite entity, non-state, non-national, establishing a discreet but omnipresent super-power, global, tentacular, with all the powers on human – and even on the vast majority of nation-states – running as zealous interpreters and executors of actions inherent to the interests of the financial system. This zeal is the responsibility of the political classes that constantly undertake bad theater, fighting their members for a place in this global power. And you don’t need to have a big intellectual brain or technical skills; it is enough to know how to please those in charge, and it is very easy to fit such a José Manuel Barroso in this profile.

The financial system has increased its discretion a lot, in proportion to its power. Decades ago, on every corner was a store open to the public, where credit operations, deposits and, cash withdrawals were carried out, in person; everything, however, in a markedly national context. Even before the internet, cash withdrawal points emerged, without a trip to bank counter, from a possession of a personalized card with a chip for this purpose, offered by the bank and later, it was charged with an annual commission.

To the extent that the capabilities of storage and traffic information were developing, especially depositors, borrowers, speculators and, swindlers, banks were losing notoriety in the streets and gaining power as credit providers, capturing individuals and businesses by increasing values in debt; and the latter has been flooding and restricting the States, which abandoned school, transportation and, housing to the gluttons of private companies. And, in parallel, the financial system has been collecting information on populations in total promiscuity with State databases.

Having information about the surrounding world, especially about the possible threats arising from it, has always been the instrument for the search for an advantage at all times, an instrument of power – in times of counties, duchies and, kingdoms, as in the subsequent nation-states. The magnates of the transition from the medieval era for the modern age lent money to monarchies but not constituted in the financial system since the creation of fit money to kings and embryonic nation-states who knew how to multiply, faking – always necessary to their aims , by reducing the gold or silver content.

Central and private banks were created to accompany the great development of colonial trade, the slave trade, war and, industrialization, expanding the monetization of national economies. The financial system received the capital resulting from looting, became internationalized, becoming an essential element in the life of nation-states, State apparatus, companies and, individuals. More recently, the creation of the euro was a decisive element in the (uneven) integration between most of the European Union’s nation-states, with the subordination of the old national central banks, made dependent on the ECB, curiously based in Frankfurt, in the nation that became the anchor of the European Union, especially after Brexit.

Nation-states were developing and deepening partnerships with each other in various fields – transport, trade, tourism, migration, education, and, military businesses and interventions … beyond monetary integration, a key element in the economic and political integration. On the other hand, the information accumulated in the financial system and its supporting technical means is an essential asset; the dependence of States, companies and, individuals on the credit offered, without much parsimony, by the financial systems, anchors consumerist habits, unreasonable indebtedness or, with amortization plans over dozens of years, with personal and material guarantees in cases of default. The dangers faced by the system are related to the contradiction between the volume of credit granted and the precariousness of debtors,especially in the face of conflict situations or crises arising from the financial system itself, as happened in 2008; and that, due to its size, required the intervention of the States, substantially increasing their levels of indebtedness and as chronic users of the fiscal punishment, ordinary or extraordinary, exercised on the peoples – to avoid greater losses for the globalized financial system, although not uniform or under a pyramidal direction.although not uniform or under a pyramidal direction.although not uniform or under a pyramidal direction.

The central objective of the financial system is to increase the volume of capital; and, its revenue is to generate capital from nothing. The balance sheet of the US Federal Reserve was in dollars, 12 * 10 ^ 11 to 8/31 2008; 49 * 10 ^ 11 on 12/31/2019 and 70 * 10 ^ 11 on last May. In the Eurozone, the corresponding items were, in euros, 4692 * 10 ^ 9 on February 28 and 6705 * 10 ^ 9 on September 2 .

All these capitals claim remuneration. And are the States, through the political classes, monitored on the top, by the financial system, which is in charge of presenting the “guides of payment” with the world population – in the form of austerity, tax hikes, unemployment, cuts in rights… keeping to a great hidden scandal, working hours equal to or greater than a hundred years ago, a time when workers fought for eight hours of work.

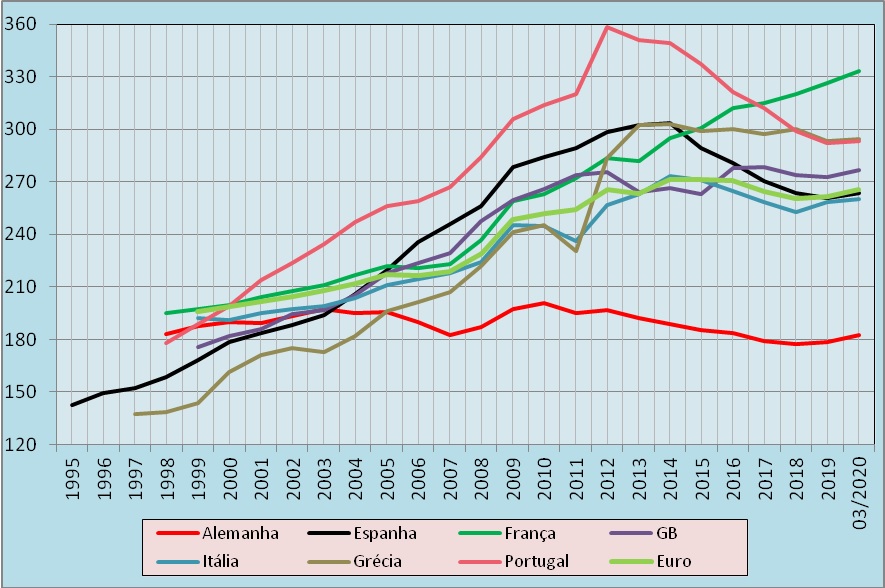

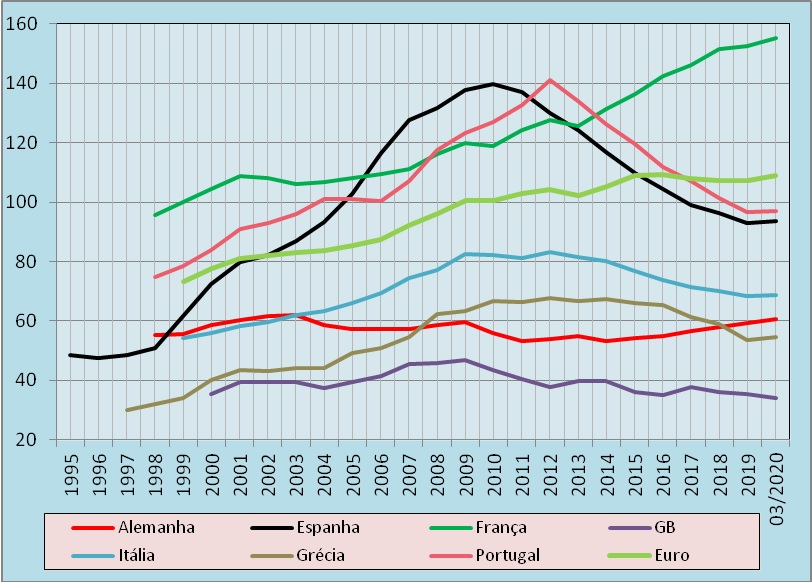

2 – Total credit directed to the non-financial sector (% of GDP)

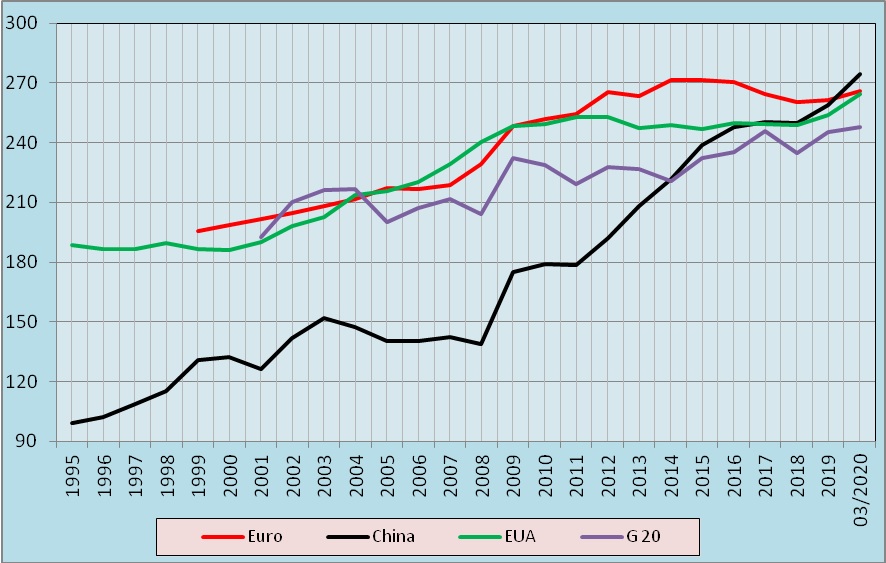

Next, we will look at several statistical series related to credit. Firstly, for some European countries and the whole of those that have euro as their currency; and for the period extending from 1995 (even without the euro in use) to March this year, the dawn of the coronavirus crisis. Second, we will observe the evolution towards large economic and population aggregates – Eurozone and G20 – and, the two largest economic powers – China and the USA.

Among the considered countries, it is observed various behaviors in the context of the whole of loans to non – financial sector; that is, the families, the State and, the companies producing goods and services.

Two situations deserve particular attention. Portuguese and German.

The credit granted by the financial sector in Portugal, in the period 1998/2012 rose from 1.8 to 3.6 times the value of GDP and whose responsibility lies essentially in the credit policy (if any) issued by the party-state, PS / PSD that has been always in power, in that period as in almost all the life of the current post-fascist regime. What stands out are the much higher levels to the average of the eurozone and other referenced countries.

The intervention of the troika and the sinking of the financial system have caused a huge drop in credit granted in the last eight years, with current levels close to those observed in 2008 (300% of GDP); and a recapitalization of banks from their dominance by foreign capital, in addition to those that were extinct or that drag on in a long and expensive agony, namely the bank we call polynomial – BES, Banco Bom, Banco Mau, Novo Banco – delivered to a vulture fund with public funding.

In the German case, there is great stability in the proportion of credit granted to families, states (central or federated), companies that produce goods and services, relating to GDP. Throughout the period, loans granted reached a maximum of 200% of GDP in 2010 and a minimum of 177.5% in 2018.

All other countries maintain strategies for marked credit growth, albeit at different levels. France maintained a great regularity in the growth of the indicator throughout the period considered, while all the others proceeded to brakes and slight setbacks, except Portugal and, as mentioned above, Spain. It is worth noting the huge relative growth of Greek debt in 2011/13, with a break in the previous period and, great stability after 2013; in return, they occured large losses in living standards and cuts in salaries and pensions.

For the large aggregates, there is a great parallel between the Eurozone and the USA, although with some distance from 2012, until recently. For China, the growth of the constituted debt is notable, from 99% of GDP in 1995 to 274.4% in March, standing ahead of the rest of the aggregates; capitalist development in a highly competitive environment requires a high degree of mimicry. It remains to be seen when the inflection or breakdown will begin, since domestic consumption in China cannot reach infinity; export Chinese may find obstacles (besides the … Trump sanctions), payment by importing countries and, the massive foreign investment, especially in the context of the Silk Routes, may find it difficult to refund the countries involved.

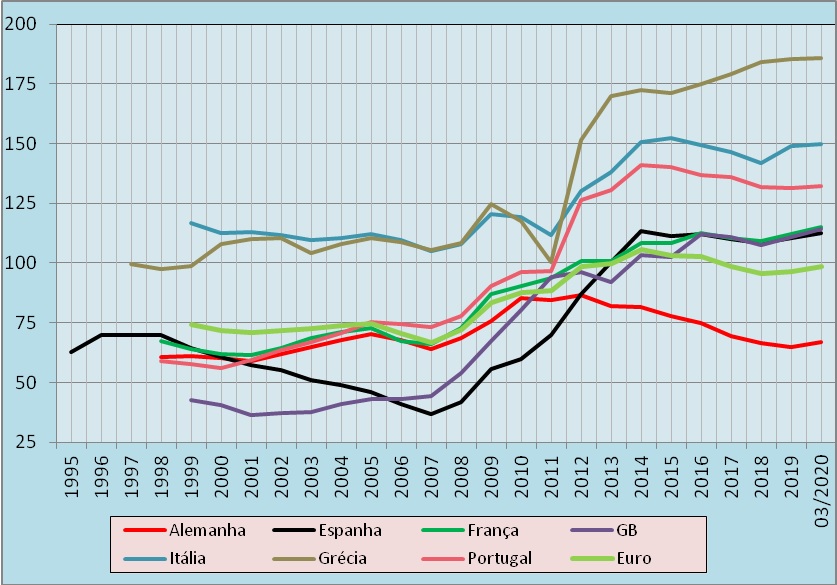

3 – Total credit granted to the public sector (% of GDP)

In the period considered, the credit granted in the eurozone to the public sector represents from 75% of GDP to the equivalent of the entire product of all euro countries.

With the Spanish exception, up to 2007 there is a great stability of the share of credit to the public sector in the global product, in the selected countries, as in the euro area as a whole. This exception corresponds in large part to the consulate of the ultra-conservative Aznar (1999-2004), which his successor Zapatero continues until 2007, with a great increase in public sector debt since then, which Rajoy has continued until 2014, from which stagnates the weight of public credit in the total GDP. As is evident, in market democracies, the economic and financial policy does not undergo major changes with the turnover between a party in power and, its twin brother in the opposition, on vacation, until a new period of application begins. with the same economic policy, with new faces.This is so evident that the reason for the elections is not even understood and, even less, the acceptance of the peoples of this rotation between corrupt gangs.

As of 2007, there has been a general increase in credit granted to the public sector, which has tended to stabilize since 2014, with the task of saving the financial system fulfilled, in the parts contained in each nation-state. The intermediate period is characterized by large growths in this debt, namely in Greece, Italy and Portugal, in addition to Spain as mentioned above; but placing the first three with much higher rates of public indebtedness from the interventions and pressures of the caretaking institutions, especially the IMF, ECB and derivatives, the EU, in some cases joined together, those, under the tenebrous name of troika .

In recent years, it is showed a chart of regularities. The highest public debt is recorded in Greece and Italy, which have that tradition; to which was added Portugal, which, in 1998, with Germany, held the lowest public debt in the table. The English case, whose neoliberalism gave in to the need to turn to the support of its financial system, showed, in 2014, a debt almost triple that recorded at the beginning of the century.

France maintains a slow growth in the weight of its public debt sector, without sudden changes. For its part, Germany starts the period under analysis with public debt compared to that of Portugal (in terms of percentage of the respective GDP’s, that is to say), reaches a maximum of 87.6% in 2010 and then decreases to stand in 2020 with slightly higher levels than 22 years ago. For those who appreciate the variety… there is a lot to choose from…

For large economic aggregates or, for the two largest powers, there is slow and smooth growth in public debt, if the period of turbulence that followed the crisis opened in 2007 is excluded. The Eurozone, after a period of initial of great stability in public indebtedness, below 80% of GDP, 2008 began a period of regular increases in indebtedness that peaked in 2014, stabilizing around the dimension of GDP since then.

The USA has maintained values similar to Those in the Eurozone since 2007, showing a large Increase in public debt Compared to the period before the crisis subprime .

Finally, China, in the 25 years shown in the graph, has evolved its public debt very slowly, from 21.2% to 58.4% of GDP, with some acceleration in recent years. However, its level of indebtedness is inferior to the Western competition, here represented by the EU and, by the US.

In the first part of this analysis, the total credit directed to the non-financial sector is accompanied by an approach on one of its installments, the public sector. In this second part, we will consider two other parts of this non-financial sector – households (including non-profit entities) and non-financial companies. Also and, as before, taking into account that all quantities are measured in terms of the percentage of GDP for each year.

Below is a schematic of the framework for the various sectors of economic activity with the data released by the Bank of International Settlements (BIS)

| Total – non-financial sector | ||||

| Public sector | Families and businesses are in profit | Companies | ||

| Non-financial private |

In today’s capitalism, it is necessary to promote increased availability of capital, since economic activity never generates sufficient income to satisfy the accumulation felt as necessary; hence the drive for economic growth that did not exist before Keynes. In this context, the aim is to increase the “invested” capital, without quantitative limitations, speculating, obtaining favors from the State, obtaining credit from the financial market (banks, stock exchange, speculation) or, making war if necessary.

On the other hand, some pressure is placed on those who live on income from consumption, largely of useless or harmful goods or services, despite the precariousness of that income. And, the satisfaction of this pressure requires the use of credit, especially in the very long term, with the financial system.

Public management itself does not escape this drive, as each gang in power needs to maintain order and obedience, domesticating police, military and, civil servants; how it needs to showcase its work to win the next elections and please the businessmen who finance the corruption of governments and political classes in general.

The way out of this common dilemma is recourse to indebtedness, something that has become obsessive and whose solution is presented by the thin capital that stands apart from the so-called “real” economy; and this, the traditional capitalists, producers of non – financial goods and services, the state apparatus, in charge of the convenient redistribution of fiscal puncture; and yet, the ordinary people, the families, the helots, whose gentleness is essential for the continuation of the capitalist system and the regimes of market “democracy”, with variable degrees of brutality.

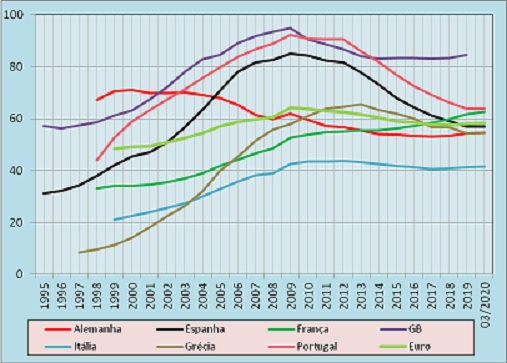

4 – Total credit directed to households and non-profit companies serving households (% of GDP)

There, in the first chart below inserted various types of credit evolution of granted or, if you prefer, the level of household debt in the last 25 years, for the chosen countries.

It is quite clear that there are two periods. The first, which ends around 2009, of a large expansion of the weight of household debt in GDP; and the second, until the present moment, in which the weight of indebtedness has stabilized.

For all euro countries as a whole, these credits grew until 2009, then retreated to the present day, clearly abandoning the high upward trend seen until the mid-decade crisis. In Britain and the Iberian countries, the household debt is very sharp, with strong growth to the discharge of the financial crisis declining thereafter, except Great Britain that keeps stable the debt burden of households in past few years.

Portugal, Spain and, Greece have large growth loans to households, and that doubles, substantially in over ten years, with Greece, at a lower level; euphoria in the Iberian countries peaked in 2009, decreasing until now to weight values in GDP close to Those recorded twenty years before. In the case of Greece, the peak is reached in 2013 but the dr op is not as sudden as in Portugal or Spain. Thus, excluding Great Britain, there is an approximation of the degree of family indebtedness in the latter, among euro countries, for indicators close to the set.

France shows a great regularity in the growth of household indebtedness and Italy shows the lowest levels of family indebtedness, compared to GDP and, in the stable plan around 40% of GDP, since 2008.

Germany shows a clear dissimilarity compared to the other countries considered. The weight of German family debts – the highest at the turn of the century – evolves until reaching the lowest coefficient, among the countries considered, with the except for Italy; a very regular evolution, with a decreasing tendency.

Synthetically, there is a clear reduction, over time, of the differences between the degree of household indebtedness to the euro countries, if Italy is excluded.

When approaching the situation for large aggregates of countries – eurozone and G20, on the one hand, and the two world colossuses – China and the USA, on the other – there is a great similarity (see graph below) between the two first aggregates, with indicators close to 60% of GDP since 2006.

As for the USA, family indebtedness had a dimension equivalent to the value of GDP in the period 2007/2009, at the height of the financial crisis known as that of subprimes. What was verified in the period reflects in negative, the debt assumption of euphoria by families with limited resources but tricked into debt increases, taking into consideration the high valuation of their homes. As the real estate lost value, unlike the debt, the execution of the mortgages led millions of people without health coverage (at the time of the enormous neglect of Trump as a political pandemic manager) and homeless, sleeping on the streets and under bridges. American Dream seems to be renaming itself American Nightmare, in the face of Xi’s smile that will be convinced of the possibility of capitalism without a hangover, protected by a new Great Wall; however,this did not prevent the Mongols from entering, let alone looting and violence carried out by barbarians (designation officially given to Europeans).

As for China, the weight in GDP of household indebtedness has sixfold in fourteen years (2006-2020), which is something extraordinary. Although it is a country with 1300 M people (two and a half times the population of the EU), it is worth asking whether a capitalist economy can maintain this rise even within the framework of tentative and intractable political power; or, if the country’s export power, even if it depends on energy and investments a little bit by all parties, can be maintained; what changes will arise from economic co-optation in the Western Pacific area (among other areas of penetration), with the Regional Comprehensive Economic Partnership. The United States’ strategic retreat in the creation of the Trans-Pacific Partnership that aimed, precisely, to leave China out, should be considered a gift to China. In return,the US has strengthened its military potential in Taiwan…

5 – Total credit directed to non-financial companies (% of GDP)

It is considered here as loans to non-financial companies, those coming from bank financing, partners or private loans, operations the stock exchange or, to public entities. As can be seen in the following graph, there are varying degrees of indebtedness taking GDP as a dynamic element of comparison.

France shows steady growth in corporate indebtedness and, always at a very high level, which reaches 155% of GDP in March of the current year; and, without a hitch in the face of the financial crisis. A regularity that, being verified with high levels of credit dependence, did not change in the trajectory during the period of financial turbulence centered in the middle of the last decade.

The Iberian countries show a huge increase in indebtedness compared to the amount of GDP, until the period when the crisis in their financial sectors is revealed, along with the deterioration of public accounts, unemployment and, the fall in activity levels. However, there is a two-year gap between the two countries concerning the turning point (Spain 2010 and Portugal, 2012). The enormous growth in indebtedness did not lead to a reinforcement of the productive capacity, nor of the purchasing power of the population, but, increment or public and private debt, as well as unemployment levels.

The enormous growth in debt resulted in a loss of purchasing power for the population and not in improvements in the quality of life. In this context, the responsibilities of the political classes are immense and it is surprisingly their disastrous performance has not led to a renewal of it, with deep changes in the model of representation. In Spain, the crisis – financial, unemployment and, evictions – generated a popular movement (15 M) in 2011 as well as a change in political chess, with the emergence of Ciudadanos, Vox and, We can let us add that the renewed movement for the separation of Catalonia or the discredit of the monarchy were elements that formally changed the political structure but not, its oligarchic and corrupt substance. In Portugal, the traditional pentapartite, continued with more or less “lonely tenors” in the Republic Assembly as well as the debt crisis or bank fraud, with deviant political provocations such as “Que Se Lixe a Troika” [1] or “Geração à Rasca” [2] , created to avoid any durable and effective contestation that would threaten the functionalism of the parliamentary “left”.

In Spain, indebtedness, in terms of GDP, almost triples in a short period of twelve years (1998/2010) while GDP itself only doubles; on the other hand, between 2010/2016 the fall in indebtedness corresponds to a period of GDP stagnation. In Portugal, indebtedness doubles compared to GDP in a slightly more extended period, of fourteen years, while the product itself stagnated in 2007/2015.

Italy and Greece correspond to the same profile mentioned above for Spain and Portugal but with much lower peaks and spaced over time, with structurally lower levels of indebtedness. For their part, Germany and Great Britain boast great regularity and much lower debt weights for non-financial companies than in France, Spain or, Portugal.

Regarding the large aggregates of countries and for the two largest powers, the USA constitutes the aggregate where the indebtedness of non-financial companies is lowest, even if with a slow rise, it reaches 78% of GDP last March.

In a general context of growth in the use of credit by non-financial companies, the regularity observed for the G20 and the Eurozone should be highlighted. There is a clear contrast with China, for which there is a strong upward trend until 2015, passing through the breaks of 2007/08 and 2009/11; in recent years, however, the use of credit by Chinese non-financial companies appears to be in restraint.

6 – Structures and dynamics in the distribution of credit / indebtedness

At this point, we intend to show, in summary, the changes regarding the main of the three major areas of credit recipients; and the duration of that top position. , for each country. At the same time, we show the average distribution of credit granted for each of the economic and social segments, also for each of the countries considered and, for all (or part) of the period to which the data refer.

| Main destinations for credit to non-financial institutions | Average distribution of credit by institutional sectors (%) | |||||

| Families | State | Companies | Families | State | Companies | |

| Germany | 1998/2004 | 2005 -> | 3 2.4 | 3 7.3 | 30.3 | |

| Spain | 1995/1999 | 2000/2014 | 26.3 | 32.4 | 41.2 | |

| 2015 -> | ||||||

| France | 1998 -> | 18.8 | 33.4 | 48.0 | ||

| Italy | 1999 -> | 15.5 | 54.0 | 30.5 | ||

| Greece | 1999 -> | 18.2 | 58.7 | 23.7 | ||

| Portugal | 2014 -> | 1998/2013 | 27.2 | 34.0 | 38.8 | |

| Z. Euro | 1999 and 2014 | 2000/2013 | 24.2 | 35.6 | 40.1 | |

| China | 2006 -> | 1 6.1 | 19.0 | 64.8 | ||

| USA | 1996/2010 | 1995/96 | 3 6.0 | 34.3 | 29.7 | |

| 2011 -> |

From the table above, are extracted the following notes related to recipients of credit or, assumed debt:

In the case of the USA, families absorbed the largest share of indebtedness until the subprime crisis put the State as the main debtor as of 2011. In 2007, the US State had a debt corresponding to 60.7% of GDP, an amount that increases regularly to 102.4% in 2012 and 111.1% in March. By contrast, household debt corresponding to 98.5% of GDP in 2007, has been declining, since up to 75.2% in March last;

In China, the preponderance of credit Obtained by companies reveals the country’s industrial and commercial strength, Especially in the area of exports; and that, contrary to typical state capitalism, economic activity develops with autonomy but obviously under the control state and the party. Note also the low share of indebtedness related to families, much lower than the so-called western countries.

taken from here

Foto: Bernhard Weber