Let us begin with the question. Why is infrastructure even important? Extensive and efficient infrastructure is critical for ensuring the effective functioning of the economy, as it is an important factor determining the location of economic activity and the kinds of activities or sectors that can develop in a particular economy. Well-developed infrastructure reduces the effect of distance between regions, integrating the national market and connecting it at low cost to markets in other countries and regions. In addition, the quality and extensiveness of infrastructure networks significantly impact economic growth and affect income inequalities and poverty in a variety of ways. A well- developed transport and communications infrastructure network is a prerequisite for the access of less-developed communities to core economic activities and services. Effective modes of transport, including quality roads, railroads, ports, and air transport, enable entrepreneurs to get their goods and services to market in a secure and timely manner and facilitate the movement of workers to the most suitable jobs. Economies also depend on electricity supplies that are free of interruptions and shortages so that businesses and factories can work unimpeded. Finally, a solid and extensive communications network allows for a rapid and free flow of information, which increases overall economic efficiency by helping to ensure that businesses can communicate and decisions are made by economic actors taking into account all available relevant information. There is an existing correlation between infrastructure and economic activity through which the economic effects originate in the construction phase and rise during the usage phase. The construction phase is associated with the short-term effects and are a consequence of the decisions in the public sector that could affect macroeconomic variables: GDP, employment, public deficit, inflation, among others. The public investment expands the aggregate demand, yielding a boost to the employment, production and income. The macroeconomic effects at a medium and long term, associated with the utilization phase are related to the increase of productivity in the private sector and its effects over the territory. Both influence significantly in the competitiveness degree of the economy. In conclusion, investing in infrastructure constitutes one of the main mechanisms to increase income, employment, productivity and consequently, the competitiveness of an economy. Is this so? Well, thats what the economics textbook teaches us, and thus governments all over the world turn to infrastructure development as a lubricant to maintain current economic output at best and it can also be the basis for better industry which contributes to better economic output. So far, so good, but then, so what? This is where social analysts need to be incisive in unearthing facts from fiction and this faction is what constitutes the critique of development, a critique that is engineered against a foci on GDP-led growth model.

Rewinding back to earlier this year in April, when the occasion was the inauguration of the 2nd annual meeting of New Development Bank (NDB) by the five member BRICS (Brazil-Russia-India-China-South Africa) countries in New Delhi, Finance Minister Arun Jaitley stressed that India has a huge unmet need for investment in infrastructure, estimated to the tune of Rs 43 trillion or about $646 billion over the next five years, 70% of which will be required in the power, roads and urban infrastructure sectors. He reiterated that in emerging markets and developing economies (EMDEs), the overall growth is picking up, although growth prospects diverge across countries. Further,

But there are newer challenges, most notably a possible shift towards inward-looking policy platforms and protectionism, a sharper than expected tightening in global financial conditions that could interact with balance sheet weaknesses in parts of the euro area and increased geopolitical tensions, including unpredictable economic policy of USA. Most importantly, the EMDEs need to carry out this huge investment in a sustainable manner. The established Multi-lateral Development Banks are now capital constrained, and with their over emphasis on processes, are unable to meet this financing challenge. We shall work with the NDB to develop a strong shelf of projects in specific areas such as Smart Cities, renewable energy, urban transport, including Metro Railways, clean coal technology, solid waste management and urban water supply.

This is the quote that reflects the policy-direction of the Government at the centre. Just a month prior to Jaitley’s address, it was the Prime Minister Narendra Modi, who instantiated the need for overhauling the infrastructure in a manner hitherto not conceived of, even though policies for such an overhauling were doing the rounds in the pipeline ever since he was elected to the position in May 2014. Modi emphasized that the Government would usher in a ‘Blue Revolution’ by developing India’s coastal regions and working for the welfare of fishing communities in a string of infrastructure projects. that such a declaration came in the pilgrim town of Somnath in Gujarat isn’t surprising, for the foundations of a smart city spread over an area of about 1400 acres was laid at Kandla, the port city. The figures he cited during his address were all the more staggering making one wonder about the source of resources. For instance, the smart city would provide employment to about 50000 people. The Blue Revolution would be initiated through the Government’s flagship Sagarmala Project attracting an investment to the tune of Rs. 8 lakh crore and creating industrial and tourism development along the coast line of the entire country. Not just content with such figures already, he also promised that 400 ports and fishing sites would be developed under the project, of which the state of Gujarat along would account for 40 port projects with an investment of about Rs. 45000 crore.

The Government, moreover plans to help the fishermen buy fishing boats at 50% subsidized rates, where five poor fishermen could form a cooperative and avail 50% subsidy and Rs 1 crore loan from Mudra scheme1. Fishermen can buy a fishing trawler with cold storage facility and increase their income (emphasis mine).

One would obviously wonder at how tall are these claims? Clearly Modi and his cohorts are no fan of Schumacher’s “Small is Beautiful” due to their obsession with “Bigger is Better”. What’s even more surprising is that these reckless followers of capitalism haven’t even understood what is meant by “Creative Destruction” both macro- or micro- economically. The process of Joseph Schumpeter’s creative destruction (restructuring) permeates major aspects of macroeconomic performance, not only long-run growth but also economic fluctuations, structural adjustment and the functioning of factor markets. At the microeconomic level, restructuring is characterized by countless decisions to create and destroy production arrangements. These decisions are often complex, involving multiple parties as well as strategic and technological considerations. The efficiency of those decisions not only depends on managerial talent but also hinges on the existence of sound institutions that provide a proper transactional framework. Failure along this dimension can have severe macroeconomic consequences once it interacts with the process of creative destruction. Quite unfortunately, India is heading towards an economic mess, if such policies are to slammed onto people under circumstances when neither the macroeconomic not the microeconomic apparatuses in the country are in shape to withstand cyclonic shocks. Moreover, these promotional doctrines come at a humungous price of gross violations of human and constitutional rights of the people lending credibility once again to the warnings of Schumacher’s Small is Beautiful: A Study of Economics as if People Mattered (emphasis mine). After this pretty long sneak peek via introduction, let us turn to Blue Economy/Blue Revolution.

Blue Economy or Blue Revolution?

What exactly do these terms mean? What is the difference between the ocean economy and the blue or sustainable ocean economy? Is it simply that a sustainable ocean economy is one where the environmental risks of, and ecological damage from, economic activity are mitigated, or significantly reduced? Is it enough that future economic activity minimizes harm to the ocean, or rather, should aim to restore its health? These are pressing questions, and thus a working definition of what blue Economy is, or rather more aptly how Blue Economy is conceived the world over is an imperative.

A sustainable ocean economy emerges when economic activity is in balance with the long-term capacity of ocean ecosystems to support this activity and remain resilient and healthy.

The ocean is becoming a new focal point in the discourse on growth and sustainable development, both at national and international levels. The world is in many ways at a turning point in setting its economic priorities in the ocean. How this is done in the next years and decades, in a period when human activities in the ocean are expected to accelerate significantly, will be a key determinant of the ocean’s health and of the long- term benefits derived by all from healthy ocean ecosystems. The idea of the “blue economy” or “blue growth” has become synonymous with the “greening” of the ocean economy, and the frame by which governments, NGOs and others refer to a more sustainable ocean economy – one, broadly, where there is a better alignment between economic growth and the health of the ocean. Increasingly, national ocean development strategies reference the blue economy as a guiding principle, while policy-makers busy themselves filling in the gaps. These gaps are very considerable. Stimulating growth in the ocean economy could be comparatively straightforward; but what is not always clear is what a sustainable ocean economy should look like, and under what conditions it is most likely to develop. It is at this point where the Government and the communities dependent on oceans for life and livelihoods come to friction, and most of the time, it is the communities which find themselves at the receiving end for whenever policies pertaining to oceans and economies thereof are blue-printed, these communities seldom have a representation, or a representational voice. As could be made amply clear from the above description of what Blue Economy entails, it is the financialization of and economics of the ocean, that gets the prerogative over pretty much everything else. Indian schema on the Blue Economy is no different, and in fact it takes the theory into a derailed practice with Sagarmala Project.

What then is Blue Revolution? As has been the customary practice of the Government of India in changing names, this ‘Revolution’ too has come in to substitute ‘Economy’ in Blue Economy. This runs concomitantly with the major principles of Blue Economy in recognizing the potential and possibilities of the fisheries sector by unlocking the country’s latent potential through an integrated approach. In the words of the Government2, the Blue Revolution, in its scope and reach, focuses on creating an enabling environment for an integrated and holistic development and management of fisheries for the socio economic development of the fishers and fish farmers. Thrust areas have been identified for enhancing fisheries production from 10.79 mmt (2014-15) to 15 mmt in 2020-21. Greater emphasis will be on infrastructure with an equally strong focus on management and conservation of the resources through technology transfer to increase in the income of the fishers and fish farmers. Productivity enhancement shall also be achieved through employing the best global innovations and integration of various production oriented activities such as: Production of quality fish seeds, Cost effective feed and adoption of technology etc.

The restructured Plan Scheme on Blue Revolution3 – Integrated Development and Management of Fisheries has been approved at a total central outlay of Rs 3000 crore for implementation during a period of five years (2015-16 to 2019-20)4. The Ministry of Agriculture and Farmers Welfare, Department of Animal Husbandry, Dairying & Fisheries has restructured the scheme by merging all the ongoing schemes under an umbrella of Blue Revolution. The restructured scheme provides focused development and management of fisheries, covering inland fisheries, aquaculture, marine fisheries including deep sea fishing, mariculture and all activities undertaken by the National Fisheries Development Board (NFDB).

The Blue Revolution scheme has the following components:

- 1 National Fisheries Development Board (NFDB) and its activities

- Development of Inland Fisheries and Aquaculture

- Development of Marine Fisheries, Infrastructure and Post-Harvest Operations

- Strengthening of Database & Geographical Information System of the Fisheries Sector

- Institutional Arrangement for Fisheries Sector

- Monitoring, Control and Surveillance (MCS) and other need-based Interventions

- National Scheme of Welfare of Fishermen

One cannot fail to but notice that this schema is a gargantuan one, and the haunting accompaniment in the form of resources to bring this to effectuation would form the central theme of this paper. Though, there is enough central assistance, the question remains: where would these resources be raised/generated? Broad patterns of Central funding for new projects broadly fall under four components,

- National Fisheries Development Board (NFDB) and its activities,

- Development of Inland Fisheries and Aquaculture,

- Development of Marine Fisheries, Infrastructure and Post- Harvest Operations and

- National Scheme of Welfare of Fishermen are as below:

- 50% of the project/unit cost for general States, leaving the rest to State agencies/ organizations, corporations, federations, boards, Fishers cooperatives, private entrepreneurs, individual beneficiaries.

- 80% of the project/unit cost for North-Eastern/Hilly States leaving the rest to State agencies/Organizations, Cooperatives, individual beneficiaries etc.

- 100% for projects directly implemented by the Government of India through its institutes/organizations and Union Territories.

Projects under the remaining three components scheme namely (i) Strengthening of Database & Geographical Information System of the Fisheries Sector, (ii) Institutional Arrangement for the Fisheries Sector and (iii) Monitoring, Control and Surveillance (MCS) and other need-based interventions shall be implemented with 100% central funding. Individual beneficiaries, entrepreneurs and cooperatives/collectives of the Union Territories shall also be provided Central financial assistance at par and equal to such beneficiaries in General States. As far as the implementing agencies are concerned, such wouldn’t really be an eye-opener.

- Central Government, Central Government Institutes/Agencies, NFDB, ICAR Institutes etc.

- State Governments and Union Territories

- State Government Agencies, Organizations, Corporations, Federations, Boards, Panchayats and Local Urban Bodies

- Fishers Cooperatives/Registered Fishers Bodies

- Individual beneficiaries/fishers, Entrepreneurs, Scheduled Castes(SCs), Scheduled Tribes (STs) Groups, Women and their Co-operatives, SHG’s and Fish Farmers and miscellaneous Fishermen Bodies.

But, there is more than meets the eye here, for Blue Revolution isn’t all about fisheries, despite having some irreparable damages caused to the fisher community inhabiting the coastline for centuries. This revolution is purported to usher in industrialization, tourism and eventually growth through a criss-cross of industrial corridors, port up gradations and connectivities, raw material landing zones, coastal economic zones through what the adversaries of Blue Economy/Revolution refer to as Ocean Grabbing.5 In order to understand the implications of what ‘Ocean Grabbing’ refers to, one must look at it in tandem with Sagarmala Project, the flagship project of the Government of India, and a case study of instantiation of Blue Economy/Revolution. Here is where we turn to in the next section.

Sagarmala

The contours of Sagarmala Project were laid out in the April 2016 perspective plan of the Ministry of Shipping. The plan involves a four-pronged approach that includes port modernization, port connectivity and port-led industrialization. It identifies Coastal Economic Zones (CEZ) and industrial clusters to be developed around port facilities mirroring the Chinese or European port infrastructure. The ambitious programmes spread across 14 ports is aimed to make domestic manufacturing and EXIM sector more competitive.

The project falls in line with Blue Revolution’s coastal community development. By “improving and matching the skills” of coastal communities, the plan seeks to ensure “sustainable development”. The plan seeks to improve the lives of coastal communities, implying that there is no contradiction between these objectives of port-led development and that of enhancing the lives of coastal residents. This seemingly win-win agenda is also endorsed by NITI Aayog’s mapping of schemes that are to help India achieve its Sustainable Development Goals (SDGs). Sagarmala is one of the ways Goal 14 will be met by 2030. Goal 14 is to conserve and sustainably use oceans, seas and marine resources.

The Kutch coast of Gujarat tops the list of potential coastal economic zones (CEZs)6 in the 2016 perspective plan. The region is not unaccustomed to the consequences of this vision of port-centred development. The environmental impact assessment (EIA) for a large port development project in Mundra, Kutch, described the lands on which the SEZ was to be set up as “non-agricultural, waste, barren or weed infested land.” But that was far from the truth. These statements have been contested by local residents through endless administrative complaints and court cases. The litigation challenging projects in coastal Gujarat have brought up elaborate arguments regarding the complex web of valuable land uses that were blotted out to make this transformation possible.

Notwithstanding the contestations over such plans for coastal land use transformation in several regions like in Kutch, the Sagarmala plan document lays out its goals as if the coast has been an empty or unproductive space, and is now poised to be a “gateway” to growth. India’s coastline currently has about 3200 marine fishing villages. Nearly half of this population (over 1.6 million people) is engaged in active fishing and fishery-related activities. While such statistics may be quoted in the plan, the official proposal views these as mere numbers or as a population that will simply toe the line and play the role assigned to them in the plan.

Port expansions involve massive dredging into the sea that destroys large stretches of fertile fishing grounds and destabilizes jetties. Fishing associations bring out a range of concerns.7 Over the years there is reduced parking space for small artisanal boats, curtailed access to fishing harbours, and unpredictable fish catch. These changes keep them in a state of permanent anxiety or turn them into cheap industrial and cargo handling labour. These families also suffer the impacts of living next to mineral handling facilities and groundwater exhaustion. India has had laws to regulate environmental impacts, but these have been mostly on paper. So, the Minister for Road Transport & Highways, Shipping and Water Resources, River Development & Ganga Rejuvenation, Nitin Gadkari’s assurances that all air and water pollution norms will be met in the implementation of the Sagarmala plan may not cut any ice with coastal dwellers. Can India afford such an imagination of ‘frictionless development’? After all, we don’t yet have a Chinese model of governance.8 Running after the Chinese model of development9 is a still a dream in the corridors of power in New Delhi.

Late last year, the Minister Nitin Gadkari exuded confidence in promoting the port-led development by confidently asserting that the project would fetch 10-15 lakh crore capital investments, generate direct and indirect employment for around two crore people and provide a huge fillip to the country’s economic growth. Gadkari, when he inaugurated the Sagarmala Development Company, a unit under his ministry, and which would act as a nodal agency for the Project said Rs 8-lakh crore investment is expected as industrial investment while an additional Rs 4 lakh crore might go into port-led connectivity. It must be noted that Sagarmala Development Company10 has Rs. 1000 crore initial-authorized capital and is registered under the Companies Act, 2013. That the Government is going ahead full steam with the implementation of the Project, howsoever ill-conceived and fuzzy it might be could be gauged by the fact that a significant portion of the Project needs to be underway till the General elections of 2019. Gadkari said that projects worth Rs 1 lakh crore under the Sagarmala programme are already under various stages of implementation and by the completion of the present dispensation’s current tenure in 2019, projects worth Rs 5 lakh crore are expected to commence. He further stressed that a national perspective plan under the Sagarmala project has been prepared and projects worth Rs 8 lakh crore have been identified. That there is a lack of transparency in garnering these funds in the public domain could easily be decipherable from what Nitin Gadkari said,

I don’t have any problem with financial resources. We have already appointed an agency to help us raise funds.

What this agency is is anyone’s guess, or maybe locating the coordinates of it is as hard as finding a needle in the haystack. But, probably, here is the clue. In order to have effective mechanism at the state level for coordinating and facilitating Sagarmala related projects, the State Governments will be suggested to set up State Sagarmala Committee to be headed by Chief Minister/Minister in Charge of Ports with members from relevant Departments and agencies. The state level Committee will also take up matters on priority as decided in the National Sagarmala Apex Committee (NSAC)11. At the state level, the State Maritime Boards/State Port Departments shall service the State Sagarmala Committee and also be, inter alia, responsible for coordination and implementation of individual projects, including through Special Purpose Vehicles (SPVs) (as may be necessary) and oversight. The development of each Coastal economic zone shall be done through individual projects and supporting activities that will be undertaken by the State Government, Central line Ministries and SPVs to be formed by the State Governments at the state level or by Sagarmala Development Company (SDC) and ports, as may be necessary.

Before getting into the financial ecosystem of Sagarmala, it is necessary to wrap this brief section on introducing Sagarmala with a list of the kinds of development projects envisaged in the initiative. This is also kind of summarizes the Blue Economy/ Revolution, Sagarmala Project and the hunger for infrastructural development by instances: (i) Port-led industrialization (ii) Port based urbanization (iii) Port based and coastal tourism and recreational activities (iv) Short-sea shipping coastal shipping and Inland Waterways Transportation (v) Ship building, ship repair and ship recycling (vi) Logistics parks, warehousing, maritime zones/services (vii) Integration with hinterland hubs (viii) Offshore storage, drilling platforms (ix) Specialization of ports in certain economic activities such as energy, containers, chemicals, coal, agro products, etc. (x) Offshore Renewable Energy Projects with base ports for installations (xi) Modernizing the existing ports and development of new ports. This strategy incorporates both aspects of port-led development viz. port-led direct development and port-led indirect development.

Table12

What does the Government want to make us believe about this ambitious Project, i.e. raison d’être for undertaking this? The growth of India’s maritime sector13 is constrained due to many developmental, procedural and policy related challenges namely, involvement of multiple agencies in development of infrastructure to promote industrialization, trade, tourism and transportation; presence of a dual institutional structure that has led to development of major and non-major ports as separate, unconnected entities; lack of requisite infrastructure for evacuation from major and non- major ports leading to sub-optimal transport modal mix; limited hinterland linkages that increases the cost of transportation and cargo movement; limited development of centers for manufacturing and urban and economic activities in the hinterland; low penetration of coastal and inland shipping in India, limited mechanization and procedural bottlenecks and lack of scale, deep draft and other facilities at various ports in India.

The Financial Ecosystem of Blue Revolution/Economy and Sagarmala Project

Let us begin with a shocker. In the words of Nitin Gadkari14,

With bank credit drying up for large infrastructure projects, the National Democratic Alliance (NDA) government is exploring a plan to raise Rs 10 trillion from retirees and provident fund beneficiaries15.

The plan aims to raise money in tranches of Rs10,000 crore by selling 10-year bonds at a coupon of 7.25-7.75%. Each tranche will be meant for a specific project. India plans to invest as much as Rs 3.96 trillion in the current financial year to bankroll its new integrated infrastructure programme which involves building of roads, railways, waterways and airports.16 It needs to be recalled that in 2015, the Government set up the National Investment and Infrastructure fund (NIIF) to raise funds for the infrastructure sector with an initial targeted corpus of Rs 40,000 crore, of which Rs 20,000 crore was to be invested by the government. The remaining Rs 20,000 crore was to be raised from long-term international investors, including sovereign wealth funds, insurance and pension funds and endowments.

Using this option is a risky affair, not that it hasn’t been used elsewhere and for a time now, but it still retains the element of risk. The risk factor is cut if the interest rates are high, for then these retiree (pension17) and provident funds are used to buy bonds that would mature when there is a need to payout. But as interest rates fall, which is very much the case with India at the moment with fluctuations and a dip in growth post-demonetization and the banking system under stress due to NPAs, these funds are likely to face up with a dilemma. Staying heavily invested in bonds would force the Government to either set aside more cash upfront or to cut promises pertaining to retiree (pension) and provident funds. If this is the two-pronged strategy of the government on one hand, then on the other, these funds, if they are allowed to raise capital from the international markets (which, incidentally is cashing and catching up in India) radically change their investment strategies by embracing investments that produce higher returns, but are staring at more risks associated with the market. Though, this shift is in line with neoliberal market policies, this has replaced an explicit cost with a hidden one, in that the policy-makers would have to channel more capital into these funds, cut back benefits or both when the stock market crashes18 causing the asset value of these funds to decline.

A project of this magnitude is generally financed using the instrument of Project Finance. So, it becomes necessary to throw light on what exactly is entailed by the term. Project Finance is looked upon as the most viable form of financing that there is with highly mitigated levels of risks, at least, according to the financial worldlings! Although, there are difficulties and challenges/needs/necessities (in short applied/application), these need to be delineated. Additionally, a study on Project Finance leads inherently to a study on Public Private Partnerships (PPPs), another preferred mode in use in India at present. One of the fundamental trade-offs for PPPs designing is to strike a right balance between risks allocations between the public and private sector, risk allocation within the private sector and cost of funding for the PPP company. This again has potentials for points of conflict with specially designed Special Purpose Vehicles (SPVs) out there to bend inclinations due to lack of disclosure clauses that define Project Finance in the first place. The factorization of PPPs and SPVs is often channeled through what is currently gaining currency the world over: Financial Intermediaries (FIs). Let us tackle these one by one in order to know the financial ecosystem that would be helpful in tracking funds and investments flowing through into the Blue Revolution/Economy and Sagarmala Project.

A project is characterized by major productive capital investment. Now, there are some asymmetric downside risks associated with a project in addition to the usual symmetric and binary ones. These asymmetric risks are environmental risks and a possibility of creeping expropriation (due to the project). Demand, price; input/supply are symmetric risks in nature, while technological glitch and regulatory fluctuations are binary risks. All that a project is on the lookout for is a customized capital structure, and governance to minimize cash inflow/outflow volatility. Project finance aims to precisely do that. It involves a corporate sponsor investing through a non-recourse debt. It is characterized by cash flows, high debt leading to a need for additional support, bank guarantees, and letters of credit to cover greater risks during construction, implementation (commissioning as the context maybe), and at times sustainability. Now funding is routed through various sources, viz. export credits, development funds, specialized assets financing, conventional debt and equity finance. This is archetypal of how the corporate financial structure operates as far as managing risks is concerned from the point of view of future inflow of funds. It has a high concentration of equity and debt ownership, with up to three equity sponsors, syndicate of banks and financial institutions to provide for credit. Moreover, there is an extremely high level of debt with the balance of capital provided by the sponsors in the form of equity, while importantly, the debt is non- recourse to the sponsors.

The attractiveness of project finance is the ability to fund projects off balance sheet with limited or no recourse to equity investors i.e. if a project fails, the project lenders recourse is to ownership of actual project and they are unable to pursue the equity investors for debt. For this reason lenders focus on the project cash-flow as this the main sources for repaying project debt. The shareholders will invest in the SPV with a focus to minimize their equity contributions, since equity commands a higher rate of return, and thus is a more risky affair compared with a conventional commercial bank debt. Whereas, the bank lenders will always seek a comfortable level of equity from shareholders of SPV to ensure that the project sponsors are seriously committed to the project and have a vested interest in seeing the project succeed.19

The figure above delineates what Project Finance could do advantageously, but at the same time is a sneak peek into what the disadvantages are.

- Project Finance mandates greater disclosure of information on deals and contracts, which happen to be proprietary in nature.

- Extensive contracting restricts management decision-making, by looping it into complexities, where decisions making nodes are difficult to make.

- Project debt is more expensive.

To turn around the disadvantages of PPPs model, an SPV is introduced. SPV is generally taken as a concessionary authority, where the concession authority is the government itself, and grants a concession to the SPV, a license granting it exclusive ownership of a facility, which, once the term for the license is over is transferred back to the government, or any other public authority. The concession forms the contract between the government and SPV and goes under the name of project agreement. Things begin to get a bit murky here, for the readers be forewarned that this applicability is becoming a commonality in the manner in which infrastructure projects are funded nowadays. Let us try and extricate the knots here.

Consider a Rs. 100 crore collection of risky loan, obligations of borrowers who have promised to repay their loans at some point in future. Let us imagine them sitting on the balance sheet of some bank XYZ, but they equally well could be securities available on the market that the Bank’s traders want to purchase and repackage for a profit. No one knows whether the borrowers will repay, so a price is put on this uncertainty by the market, where thousands of investors mull over the choice of betting on these risky loans and the certainty of risk-free government bonds. To make them indifferent to the uncertainty these loans carry, potential investors require a bribe in the form of 20% discount at face value. If none of the loans default, investors stand a chance to earn a 25% return. A good deal for investors, but a bad one for the Bank, which does not want to sell the loans for a 20% discount and thereby report a loss.

Now imagine that instead of selling the loans at their market price of Rs. 80 crore, the Bank sells them to an Special Purpose Vehicle (SPV) that pays a face value of Rs. 100 crore. Their 20% loss just disappeared. Ain’t this a miracle? But, how? The SPV has to raise Rs. 100 crore in order to buy the loans from the Bank. Lenders in SPV will only want to put Rs. 80 crore against such risky collateral. The shortfall of Rs. 20 crore will have to be made up somehow. The Bank enters here under a different garb. It puts in Rs. 20 crore as an equity investment so that the SPV has enough money now to buy the Rs. 100 crore of loans. However, there is a catch here. Lenders no longer expect to receive Rs. 100 crore, or a 25% return in compensation for putting up the Rs. 80 crore. SPV’s payout structure guarantees that the Rs. 20 crore difference between face value and market value will be absorbed by the Bank, implying treating Rs. 80 crore investment as virtually risk-free. Even though the Bank has to plough Rs. 20 crore back into the SPV as a kind of hostage against the loans going bad, from Bank’s perspective, this might be better than selling the loans at an outright Rs. 20 crore loss. This deal reconciles two opposing views, the first one being the market suspicion that those Bank assets are somehow toxic, and secondly that the Bank’s faith that its loans will eventually pay something close to their face value. So, SPVs become a joint creation of equity owners and lenders, purely for the purpose of buying and owning assets, where the lenders advance cash to the SPV in return for bonds and IOUs, while equity holders are anointed managers to look after those assets. Assets, when parked safely within the SPV cannot be redeployed as collateral even in the midst of irresponsible buying spree.

Now, this technically might spell out the reasons for why an SPV is even required in the first place. But, enter caveat, for the architecture of an SPV is what lends complexity and a degree of murkiness to it. If one were to look at the architecture of SPV holdings, things get a bit muddled in that not only is the SPV a limited company registered under the Companies Act 2013, the promotion of SPV would lie chiefly with the state/union territory and elected Urban Local Body (ULB) on a 50:50 equity holding. The state/UT and ULB have full onus to call upon private players as part of the equity, but with the stringent condition that the share of state/UT and ULB would always remain equal and upon addition be in majority of 50%. So, with permutations and combinations, it is deduced that the maximum share a private player can have will be 48% with the state/UT and ULB having 26% each. Initially, to ensure a minimum capital base for the SPV, the paid up capital of the SPV should be such that the ULB’s share has an option to increase it to the full amount of the first installment provided by the Government of India. There is more than meets the eye here, since a major component is the equity shareholding, and from here on things begin to get complex. This is also the stage where SPV gets down to fulfilling its responsibilities and where the role of elected representatives of the people, either at the state/UT level or at the ULB level appears to get hazy. Why is this so? The Board of the SPV, despite having these elected representatives has in no certain ways any clarity on the decisions of those represented making a strong mark when the SPV gets to apply its responsibilities. SPVs, now armed with finances can take on board consultative expertise from the market, thus taking on the role befitting their installation in the first place, i.e. going along the privatization of services in tune with the market-oriented neoliberal policies. Such an arrangement is essentially dressing up the Economic Zones in new clothes sewn with tax exemptions, duties and stringent labour laws in bringing forth the most dangerous aspect of Blue Revolution/Economy/Sagarmala Project, viz. privatized governance. In short, this is how armed with finances, the doctrine of privatized governance could be realized, and SPV actually becomes the essence to attain it.

Turning our focus to what is often termed the glue in Project Finance, the instrument widely practiced today and what often joins PPPs and SPVs into a node of financing, Financial Intermediaries. Although, very much susceptible to abuse for the way it has been implemented, these are institutions that provide the market function of matching borrowers and lenders or traders. Financial intermediaries facilitate transactions between those with excess cash in relation to current requirements (suppliers of capital) and those with insufficient cash in relation to current requirements (users of capital) for mutual benefit. Now these take on astronomical importance considering that almost every other Non-Banking Financial Institution or an SPV could potentially be a financial intermediary. For example, insurance companies, credit unions, financial advisors, mutual funds and investment trusts are financial intermediaries. Financial intermediaries are able to transform the risk characteristics of assets because they can overcome a market failure and resolve an information asymmetry problem. Information asymmetry in credit markets arises because borrowers generally know more about their investment projects than lenders do. The information asymmetry can occur “ex ante” or “ex post”. An ex ante information asymmetry arises when lenders cannot differentiate between borrowers with different credit risks before providing loans and leads to an adverse selection problem. Adverse selection problems arise when an increase in interest rates leaves a more risky pool of borrowers in the market for funds. Financial intermediaries are then more likely to be lending to high-risk borrowers, because those who are willing to pay high interest rates will, on average, be worse risks. The information asymmetry problem occurs ex post when only borrowers, but not lenders, can observe actual returns after project completion. This leads to a moral hazard problem. Moral hazard arises when a borrower engages in activities that reduce the likelihood of a loan being repaid. An example of moral hazard is when firms’ owners “siphon off” funds (legally or illegally) to themselves or to associates, for example, through loss-making contracts signed with associated firms.

The problem with imperfect information is that information is a “public good”. If costly privately-produced information can subsequently be used at less cost by other agents, there will be inadequate motivation to invest in the publicly optimal quantity of information. The implication for financial intermediaries is as follows. Once banks obtain information they must be able to signal their information advantage to lenders without giving away their information advantage. One reason, financial intermediaries can obtain information at a lower cost than individual lenders is that financial intermediation avoids duplication of the production of information. Moreover, there are increasing returns to scale to financial intermediation. Financial intermediaries develop special skills in evaluating prospective borrowers and investment projects. They can also exploit cross- sectional (across customers) information and re-use information over time. Adverse selection increases the likelihood that loans will be made to bad credit risks, while moral hazard lowers the probability that a loan will be repaid. As a result, lenders may decide in some circumstances that they would rather not make a loan and credit rationing may occur. There are two forms of credit rationing: (i) some loan applicants may receive a smaller loan than they applied for at the given interest rate, or (ii) they may not receive a loan at all, even if they offered to pay a higher interest rate.

In other words, financial intermediaries play an important role in credit markets because they reduce the cost of channelling funds between relatively uninformed depositors to uses that are information-intensive and difficult to evaluate, leading to a more efficient allocation of resources. Intermediaries specialize in collecting information, evaluating projects, monitoring borrowers’ performance and risk sharing. Despite this specialization20, the existence of financial intermediaries does not replicate the credit market outcomes that would occur under a full information environment. The existence of imperfect, asymmetrically-held information causes frictions in the credit market. Changes to the information structure and to variables which may be used to overcome credit frictions (such as firm collateral and equity) will in turn cause the nature and degree of credit imperfections to alter. Banks and other intermediaries are “special” where they provide credit to borrowers on terms which those borrowers would not otherwise be able to obtain. Because of the existence of economies of scale21 in loan markets, small firms in particular may have difficulties obtaining funding from non-bank sources and so are more reliant on bank lending than are other firms. Adverse shocks to the information structure, or to these firms’ collateral or equity levels, or to banks’ ability to lend, may all impact on firms’ access to credit and hence to investment and output.

This section started with a shocker, and then weaved the plot generically in a deliberate manner to highlight the financial instruments in use for funding the massive Blue Revolution/Economy and Sagarmala Project. From the generic sense, it is time to move on to the specifics, where in the next section, one could easily fathom the generic nature of these instruments in use. this section was indeed technical, but a major collaborator to understanding the contours of Project Finance, and how is it that such instruments govern the polity and the policy of the ruling dispensation. Let us therefore, turn to what engineers the funding of this infrastructural giant.

Engineering Finance for Blue Revolution/Economy and Sagarmala Project

To reiterate, at the Central level, the Sagarmala Development Company (SDC) has been set up under the Companies Act, 2013 to assist the State level/zone level Special Purpose Vehicles (SPVS), as well as SPVs to be set up by the ports, with equity support for implementation of projects under Sagarmala to be undertaken by them. The formation of SDC was approved by the Cabinet on 20th July 2016 and was incorporated on 31st August 2016. It may be clarified that the implementation of the projects shall be done by the Central Line Ministries, State Governments/State Maritime Boards and SPVs and the SDC will provide a funding window and/or take up only those residual projects that cannot be funded by any other means/mode. The SDC will primarily provide equity support to the State-level or port-level SPV. All efforts would be made to implement these projects through the private sector and through the Public Private Participation (PPP) wherever feasible, strictly following the established guidelines and modality of appraisal and sanction of PPP projects. Projects in which SDC will take an equity stake, are expected to start giving returns only after 5-6 years. Therefore, SDC will be supported during initial 5-6 years through budgetary allocation of Ministry of Shipping. SDC will also be raising funds as debt/equity (as long term capital) from multi-lateral and bilateral funding agencies, as per the requirements, in consultation with Department of Economic Affairs. The SPVs in which SDCL will invest may start giving dividends once they become profitable and will constitute a revenue stream. The expenses incurred for project development will be treated as part of the equity contribution of SDC. In case SDCL is not taking any stake or the expenses incurred are more than the stake of SDC, then it will be defrayed by the SPV to SDC. SDC may, in future, want to divest its investment in any particular SPV to recoup its capital for future projects. At the State level, the State Maritime Boards/State Port Departments shall service the State Sagarmala Committees and also be, inter alia responsible for coordination and implementation of individual projects, including through SPVs and oversight. The State Governments/State Maritime Boards (SMBs) shall implement such identified projects either from their own budgets or through SPVs wherein the SDC may provide equity support, as may be required and necessary. Funds will be sought for the implementation of residual projects from time to time in the budgets of the respective ministries/departments which will be implementing the projects. The Ministries/State Governments/Maritime Boards shall implement such identified either from their own budgets or through SPVs wherein the SDC may provide equity support, as may be required and necessary. Projects considered for funding (other than equity support) under Sagarmala’s budget shall be appraised and approved under the extant instructions and guidelines of the Ministry of Finance. Road and rail connectivity projects, already appraised and approved by the Ministry of Road Transport & Highways and Ministry of Railways respectively, will be considered as appraised projects. A representative of Ministry of Shipping could be a member of the project appraisal committee, set up by the relevant Ministries. Projects considered for equity support under Sagarmala and to be financed by SDC, will be independently appraised and approved by SDC as per its procedure. One can see that even if the title of the section is engineering, it is actually the architecture of who gets to fund what that is slowly building up the complexity of Sagarmala. Let us take a brief look at the numbers before getting back to engineering of funding.

As of March 2017, under Sagarmala, 415 projects, at an estimated investment of approximately Rs. 8 lakh crore, have already been identified across port modernization & new port development, port connectivity enhancement, port-linked industrialization and coastal community development for phase wise implementation over the period 2015 to 2035. As per the approved implementation plan of Sagarmala, these projects are to be taken up by the relevant Central Ministries/Agencies and State Governments preferably through private/PPP mode.

Some of the key projects are:

- Rs. 58.5 Crore released for capital dredging for Gogha-Dahej RO-Pax Ferry Services project

- Rs. 50 Crore released for construction of RoB cum Flyover at Ranichak level crossing at Kolkata Port

- Rs. 43.76 Crore released for RO-RO Services Project at Mandwa

- Rs. 20 Crore released for setting up second rail line from Take-off Point A cabin atDurgachak (Haldia Dock Complex)

- Rs. 20 Crore released for Vizag Port road connectivity to NH5

- Rs. 10 Crore released for development of a full-fledged Truck Parking Terminal adjacent to NH7A (VOCPT)

As part of the Sagarmala Programme, 6 new port locations have been identified, namely – Vadhavan, Enayam, Sagar Island, Paradip Outer Harbour, Sirkazhi and Belekeri. The current status of each of the proposed new port locations is as follows:

Increasing the share of coastal shipping and inland navigation in the transport modal mix is one of the key objectives of Sagarmala. In order to equip ports for movement of coastal cargo, the scope of coastal berth scheme has been expanded and merged with Sagarmala. Under the scheme, the financial assistance of 50% of project cost is provided to Major Ports/State Governments for construction of Coastal Berths, Breakwater, mechanization of coastal berths and capital dredging. Rs. 152 Cr has been released for 16 projects under this scheme. To augment transshipment capacity in the country, Vizhinjam (Kerala) and Enayam (Tamil Nadu) are being developed as transshipment ports. Vizhinjam is being developed as transshipment hub under PPP mode by Government of Kerala with Viability Gap Funding22 from Government of India.

Switching back to engineering, projects considered for funding under Sagarmala will either be provided equity support (SPV route) from SDC or funded (other than equity support) from the budget of Ministry of Shipping. Port projects will be primarily funded through the SPV route. Once the project is funded after due appraisal and approval, to the extent and limits prescribed under the guidelines, funds shall be released once all the clearances are in place. Most importantly, no other guarantees23 will be provided to the projects considered for funding.

The fund contribution from Sagarmala (from the budget of Ministry of Shipping) in any project will be limited to 50 per cent of project cost as per the Detailed Project Report (DPR) or tendered cost, whichever is lesser. 50 per cent is the cap of assistance from all sources/schemes of Government of India and will be provided in three tranches24 based on project milestones, In case of UTs, where no other sources of funding are available, the limit of 50 per cent could be relaxed. The fund released for a project being implemented in convergence mode with the schemes of other Central Line Ministries will not be higher than the approved ceiling of financial assistance under the concerned Central Sector Scheme (CSS). Projects having high social impact but with no return or low Internal Rate of Return (IRR)25 (e.g. fishing harbour projects, coastal community skill development projects, coastal tourism infrastructure projects etc.) may be provided funding, in convergence with the schemes of other Central Line Ministries, for implementation under Engineering, Procurement and Construction (EPC) mode. EPC mode is an interesting digression from PPP model as the former has a slight edge over the latter. In an EPC mode, the Government bears the entire financial burden and funds the project by raising capital through issuing bonds. In PPP, private entity would do cost-benefit analysis and would bid for project. Cheapest bid would be selected. So incentive is to reduce bid price. But as construction starts, there are local protests against land acquisition, and thus work halts. That means now costs would go up. Project faces market risk. Private entity will suffer loss and would refuse to work on pre-agreed bid. He would ask for more funding from Government. Government machinery, lethargic or may be skeptic of bidder’s intentions, would also make counter-arguments. And so there would be litigations. In EPC, it is government who is going to take up engineering. But, does government has engineering expertise? No, so government would call for bids for engineering knowledge. Thereafter, the government would give out calls for procurement of raw material and construction expertise. Under an EPC contract, the contractor designs the installation, procures the necessary materials and builds the project, either directly or by subcontracting part of the work. In some cases, the contractor carries the project risk for schedule as well as budget in return for a fixed price, called lump sum or LSTK26 depending on the agreed scope of work. So here, if project halts due to say local protests, government will deal with it. The private entity is saved from political questions. Anyway private entities are there merely for bottomline, whereas government is there for political tussle and governance. Thus EPC makes more sense and is an alternative for PPP. But, barring a few exceptions, the Government is still holding on to PPP as the preferred mode.

The equity contribution from SDC, in any project SPV, will be decided based on the project equity as per its DPR and will generally not exceed 49 per cent of the project equity. SDC can take equity contribution in existing or newly incorporated SPVs formed by State Governments/Maritime Boards/Ports etc. provided that these SPVs have projects which are ready for implementation. SDC can take equity in an existing or newly incorporated umbrella SPVs formed by State Governments/Maritime Boards/Ports etc. provided the same has been duly approved by the competent authority. SDC’s participation in the umbrella SPV would not restrain SDC from taking part in any other project SPV created by the same State Governments/Maritime Boards/Ports. SDC shall take only token equity to initiate/assist the process of project development in those SPVs which are scouting for projects or having projects under development stage only. As it would be difficult to ascertain the revenue flow from a particular project, a separate accounting for each project is an important clause in the contract document of the SPV. Continuing in line with equity-based funding, the question then arises as to what would be the recommended monitoring parameters for funded projects for equity and for those other than equity? Projects which are provided equity support (SPV route) by SDC will be monitored by the SPVs as well as SDC and Ministry of Shipping through an appropriate monitoring and evaluation mechanism. For projects which are provided funding (other than equity support), the fund recipients/project proponents will submit monthly progress report (physical and financial) of projects as per the electronic format/ MIS prescribed by SDC. SDC along with the fund recipients/project proponents will monitor the progress of projects based on the same. Additionally, the fund recipients/ project proponents will submit the utilization certificate for the fund released in the previous tranche for claiming release of subsequent installments/tranches. Wherever possible, the fund recipients/project proponents will submit a completion certificate, issued by an independent 3rd party agency, along with the final utilization certificate to claim the final tranche of fund. The 3rd party agency is to be appointed by the Ministry of Shipping from the approved panel maintained by the Indian Ports Association (IPA) for this purpose. The cost of appointing and functioning of the 3rd party agency will be borne by the Ministry of Shipping. The fund recipients/project proponents will maintain financial records, supporting documents, statistical records and all other records, to support performance of the project.

Although the monitoring mechanisms look neat on paper, there is absence of any transparency and accountability of whether these are in existence, or are these to be invoked at a stage when funds reach a point of questionability either in the sense of non- repayment, or by stressed assets, the consequent of which are the Non-Performing Assets. Still, what is not very clear is who are the funders involved apart from Government of India and State Governments. It is absolutely clear though, that both these entities would be taking recourse to National Financial Institutions (NFIs) and Non-Banking Financial Institutions (FIs) in addition to packing coffers in the budgets (both at the central and at the state levels) towards the massive investments in point. But, what of the International Financial Institutions (IFIs), or bi-lateral development institutions? This question is slightly jumping the gun, and would be understood in the perspective of what has now come to be called Blue Growth Initiative (BGI). Let us park this for a section and turn to looking at Sagarmala with some of its humungous initiatives that would give an idea behind numbers and figures.

Multi-headed Hydra (Projects envisaged under Sagarmala)

That the Government is going full steam on infrastructure cannot be fathomed by looking at Sagarmala in isolation. This has to be looked in tandem with industrial corridors, coastal economic zones, inland waterways, and tourism among a host of infrastructural stressed-upon points. Though, much of that is largely outside the scope of this chapter, it nevertheless is crucial to hover the compass of analysis in a loci around these allied infrastructures.

Starting with port modernization and new port development, Sagarmala is a gamut of 189 projects tipped at a whopping 1.42 lakh crore. Of these, the masterplans have already been finalized for 12 major ports; 142 projects at a cost of Rs. 91, 434 crore identified for implementation till 2035; and 42 projects worth Rs. 23, 263 crore are already under implementation.

Port modernization along with new port development and major port operational efficiency improvement is to be integrated into what is now referred to as promotion of cruise tourism, foe which a task force has already been constituted and where now foreign flag vessels with passengers on board would be allowed to call at Indian ports without obtaining a license from director General of Shipping. Well, isn’t this what globalization is all about? Yes, largely, and more concertedly if the operating procedures effectuating these get standardized, and this is what has precisely happened for promoting cruise tourism in consultation with Bureau of Immigration, Ministry of Home Affairs, Central Board of Excise and Customs, Central Industrial Security Force and Port Authorities. The collaborative efforts of these authorities have led to the constitution of port-level committees to address manpower, coordination and logistical support. It is under the aegis of Sagarmala that cruise terminals are under development at Chennai and Mormugao in Goa.

Under the umbrella of port connectivity enhancements, 170 projects are either approved or in the pipeline at a cost of Rs. 2.3 lakh crore comprising of rail connectivity projects, road connectivity projects, multi-modal logistics parks and coastal shipping. Rail and road connectivity are precisely the components of freight corridors also launched under the name of industrial or economic corridors. Coastal shipping on the other hand is closely amalgamated with inland waterways. On a project-wise scale, there are plans to implement road projects under Sagarmala including 10 freight friendly expressways (E.g. Expressway from Ahmedabad to JNPT). Other proposals include awarding implementation of Heavy Haul Rail Corridor project between Talcher & Paradip in coordination with Ministry of Railways, proposing Cabotage relaxation for 2 years subject to level playing field for Indian flag ships, and bringing out a modal shift incentive scheme for Inland Water Transport sector by developing 37 prioritized National Waterways.

On the port-led industrialization front, 33 projects are either approved, or in the pipeline at a cost of Rs. 4.2 lakh crore with perspective plans prepared for 14 coastal economic zones (CEZs). Moreover, 29 potential port-linked industrial clusters identified across Energy, Materials, Discrete Manufacturing and Maritime sectors are identified. The futuristic plans for port-led industrialization involves developing master plans for the 14 coastal economic zones in a phased manner with the first phase covering the states of Gujarat, Maharashtra, Andhra Pradesh and Tamil Nadu. The proposals also include developing detailed project reports (DPRs) for maritime clusters in Gujarat and Tamil Nadu. Crucially, the integration of smart cities with Sagarmala would be the implementation of Kandla & Paradip Smart Port Industrial Cities. What the Government has achieved through the New Shipbuilding Policy is granting shipyards infrastructure status, thus helping avail cheap working capital. The policy also has provided exemptions on taxes and duties, and made recommended arrangement for financial assistance to the tune of Rs. 20 crore of the initial cost flowing in from the center.

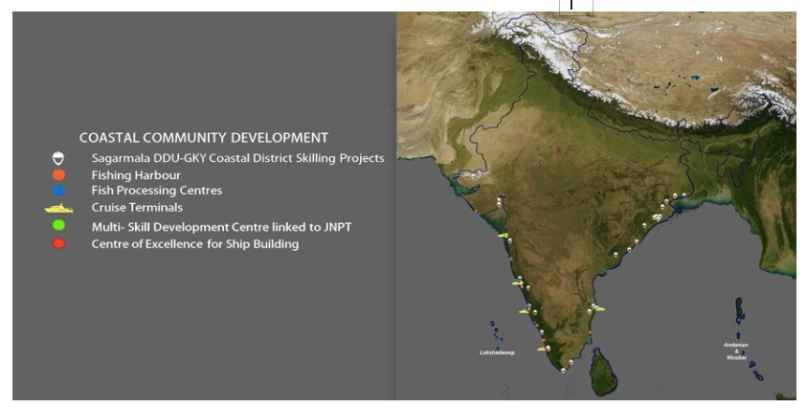

The Coastal Community Development could be looked at under two broad categories, viz. skill development and fisheries development. Under the category of skill development, Rs. 30 crore have been sanctioned, of which Rs. 10 crore are already released towards safety training for workers in Alang-Sisoya shipyard. For the Coastal Districts Skill Training Project under Deen Dayal Upadhyay Grameen Kaushal Yojana (DDU-GKY), Rs. 13.77 crore have been sanctioned & Rs. 6.9 crore are already released. The Ministry of Shipping is undertaking skill gap analysis in 21 coastal districts, and the action plan for 6 districts in Gujarat, Maharashtra & AP are already prepared with projects from the same to be implemented under DDU-GKY. Under fisheries development, the Ministry of Shipping is part-funding select fishing harbour projects under Sagarmala in convergence with Department of Animal Husbandry Dairying & Fisheries (Ministry of Agriculture). On a more specific project-wise data, Rs. 52.17 crore is sanctioned for modernization & upgrading of Sassoon Dock. Upgradation of Kulai, Veraval and Mangrol fishing harbours are in the pipeline. For the Ministry of Shipping, this would support development of deep sea fishing vessels and fish processing centers in convergence with Department of Animal Husbandry Dairying & Fisheries.

The scale is massive and thus makes the moot question of who is financing Sagarmala all the more pressing. The disclaimer is: not much is known as there is a tremendous lack of transparency and accountability as regards this. But, information from discrete sources that are in the public domain at least gives a fair enough idea of who could be behind this gigantic infrastructure? At the same time, one needs to look at the intricate knot between the financiers and Blue Growth Initiative to draw out a clear message, which shouldn’t be shocking anymore, and that being the policies and funds are internationally-oriented. It is this section, the penultimate one in the chapter that we now turn to.

Who possibly could be driving the impetus for Blue Revolution/Economy and Sagarmala?

Are there International Financial Institutions involved? Hopefully by the end of this section, there would be some clarity to the muddied waters. Shipping ministry is roping in global multilateral agencies to extend a helping hand to entrepreneurs looking to explore Rs 3.5 lakh-crore of investment opportunities under the Sagarmala project, which was aimed at port-led development along 7,500-km coastline. Devendra Kumar Rai, Director at the Ministry of Shipping, said Sagarmala Development Company, with an equity base of Rs 1,000 crore, would chip in for investments and viability gap funding to help entrepreneurs achieve viable returns on their investments. He also said that the company was also seeking the support of Asian Development Bank (ADB) and other multilateral agencies for program loans to various initiatives under the Sagarmala project.27 Admitting that not all the projects being contemplated under the Sagarmala project would offer attractive returns on investments, Rai said, “The shipping ministry views that unless there is at least 13 per cent IRR, no private investor would come forward to invest.” To address the issue of not so attractive returns, the ministry would encourage some projects under the public-private partnership model and even extend the viability gap funding (VGF) up to 40 per cent of the project cost to turn the projects viable, Rai said. MT Krishna Babu, chairman of Visakhapatnam Port Trust, said various development projects will be thrown open for private participation. “The five greenfield ports alone would involve investments of around Rs 25,000 crore each in phases.” Babu said it will mobilise funds from government and global agencies like ADB and Japan International Cooperation Agency (JICA) and decide on the nature of funding to the unviable projects – whether equity or VGF.28

Asian Development Bank (ADB) has been giving boosters to India’s infrastructure development program from time to time, and injected yet another towards the end of June this year, when it promised the country its commitment to investing $10 billion over the next five years. Half the sum, or $5 billion were to be used for developing the 2,500 km East Coast Economic Corridor, which will ultimately extend from Kolkata to Tuticorin in Tamil Nadu. ADB had last year approved $631 million to develop the 800-km industrial corridor between Visakhapatnam and Chennai.29 The East Coast Economic Corridor also aligns with port-led industrialization under Sagarmala initiative and Act East Policy by linking domestic companies with vibrant global production networks of east and southeast Asia.

The World Bank, on the other hand, might not seem to have a direct hand in the funding of Sagarmala, but thinking it thus would be like missing the woods for the trees. Though the Bank is heavily investing in industrial corridors with a significant share in Amritsar-Kolkata Industrial Corridor, and seed capital along with creating conditions ripe for Viability Gap funding along the Delhi-Mumbai Industrial corridor, its involvement in Sagarmala is like an advisory to the Government of India. The World Bank, which has been advising the shipping ministry on the development of the inland waterways and the Clean Ganga mission, has approved an assistance of Rs 4,200 crore for the development of the existing five national waterways. Incidentally, India has jumped 19 places in the latest World Bank ranking in the global logistics performance. The World Bank in its latest once-in-two-year Logistics Performance Index (LPI) said India is now ranked 35th as against the 54th spot it occupied in the previous 2014 report. Such rise in position on the global logistics performance is the policy shot in the arm for India, thus making it conducive for investments to flow in.

But, to understand the policy initiatives behind Blue Revolution/Economy and Sagarmala, one needs to keep a tab on what is known as the Blue Growth Initiative, which happens to be the climate initiatives platform of the United Nations Programme on Environment. The Food and Agriculture Organization of the United Nations (FAO) Blue Growth Initiative (BGI) aims at building resilience of coastal communities and restoring the productive potential of fisheries and aquaculture, in order to support food security, poverty alleviation and sustainable management of living aquatic resources. Promoting international coordination is crucial to strengthen responsible management regimes and practices that can reconcile economic growth and food security with the restoration of the eco-systems they sustain. The initiative works towards two major goals, viz.

- Enabling environment (capacity building, knowledge platform, and improved governance) established within 2 to 3 years in 10 target countries.

- 10% reduction of carbon emissions in the 10 target countries in 5 years and 25% in 10 years.

- 3. Reduction of overfishing by 20% in the target countries in 5 years and 50% in 10 years.

- 4. “Blue communities” established in 5 target countries and resource stewardship ownership with 30% improved livelihoods.

- 5. Ecosystem degradation reversed in the target countries and 10% ecosystems restored in 4 target countries within 5 years.

These goals are to be attained by improving the evaluations of ecosystem services in Large Marine Ecosystems including coastal zones and Lakes for local and regional integrated and spatial planning. Also, strengthened fisheries and aquaculture governance and institutional frameworks would augment clear objectives and development paths for the sector; by increasing contributions from the small-scale fisheries and aquaculture sectors – through improved fisheries management, aquaculture development and improved post-harvest practices and market access. The initiative plans to attain increased resilience to climate change, extreme events and other drivers of change through improved knowledge of vulnerability and adaptation and disaster risk management options specific to fisheries, aquaculture and dependent communities who are at the front line of change and thereby providing technical and financial support to transitioning the sector to low-impact and fuel/energy efficiency and Blue Carbon enhancements30. for the medium and long term, the BGI is being promoted as an important vehicle for mobilizing resources and advocacy in international fora. In the global arena, the Initiative is enabling FAO to align with major global initiatives such as the Green Economy in a Blue World (UNEP/IMO/FAO/UNDESA/IUCN/World Fish), the Global Partnership for Oceans GPO (World Bank), the Coral Triangle Initiative, the Oceans SDG, Fishing for the Future (World Fish/FAO), the World Ocean Council and GEF6, as well as commitments stemming from the Rio+20 Conference. The oceans with a current estimated asset value of USD 24 trillion and an annual value addition of US$2.5 trillion, would continue to offer significant economic benefits both in the traditional areas of fisheries, transport, tourism and hydrocarbons as well as in the new fields of deep-sea mining, renewable energy, ocean biotechnology and many more, only if integrated with sustainable practices and business models. With land-based resources depleting fast, there are renewed attempts to further expand economic exploitation of the world’s oceans. However, if not managed sustainably, growing economic engagement with the oceans could risk further aggravation of their already strained health with serious impact on their natural role as the single most important CO2 sink and replenisher of oxygen. This in turn could accelerate global warming with catastrophic effects on fish stocks, climatic stabilization, water cycle and essential biodiversity. With arguments like these, UNFAO sure needs voices from the communities who would be severely impacted by these policies slapped on them.

So, even if India is not officially a participating nation in the Blue Growth Initiative (BGI), it could easily be drawn that the whole rationale for the Blue Revolution has sprung up from UNFAO. So, what is the viability of Blue Revolution/Economy and Sagarmala? It is to this section we turn now by way of conclusion.

Conclusion

Even while this chapter was being written, another mega infrastructure project in the form of country’s first bullet train was inaugurated to be laid between the Financial Capital Mumbai and Ahmedabad. As Prime Minister Narendra Modi and Japanese Prime Minister Shinzo Abe lay the foundation stone for the Mumbai-Ahmedabad bullet train project in Gujarat, tribals in Maharashtra and Gujarat will meet tehsildars of tribal areas that will be impacted by the project and submit letters of protest.31 Criticisms of the kind are expected and are already taking shape across the coastline.32 But, since this chapter is geared towards understanding the financial and economic ecosystem of Blue Revolution/ Economy and Sagarmala, let us divert our attention to financial critiques of mega infrastructural development projects.

The corporates and multinational Companies have joined together with the intention to grab the ocean and the coast. State and Central governments have become agents of the corporates and are permitting the foreign trawlers in the India deep seas, constructing atomic thermal power stations, disastrous chemical industries, hotels and big resorts and coastal industrial corridors at the coasts. These projects have several illegalities in formulation, approval, sanction and implementation. The livelihood of the fishworkers has not been considered by the elected government.33 The corporates have freedom to pour toxic affluent in the coastal area and sea soar. As a result fishes died and disappeared. So far more than twenty commercial species of fish have been disappeared from the sea at Kachchh, Gujarat. Similar is the case in other sea areas. Mangroves have been destroyed and land are being used by corporates. Solid toxic wastes and inflatable toxics dumped in forest and other empty threatens human and animal lives in the coastal area.34 This is not a mirror into the post-apocalyptic, run over by hungry capitalism scenario, but a reality that is very much brewing across the coastline of the country from Gujarat in the west to West Bengal in the east.

Economically and financially, there are three major challenges that are encountered in infrastructural mega-projects. In one influential study, Bent Flyvbjerg35, an expert in project management at Oxford’s business school, estimated that nine out of ten go over budget. Second challenge is the time overrun, which directly leads to cost escalation. Finally, the premise that projects need to work on two levels – in the short term for recovering financial outlays and the longer term for creating social impact – often becomes a barrier to taking action. Even projects that are needed do not get executed, especially in places where revenues from a project are unlikely to cover its cost. the enormity of Sagarmala leaves it vulnerable to unviability. In addition to three reasons cited above as to what could challenge a mega-project, these three reasons are most likely to be attributable to why Sagarmala could remain an unfinished dream, and in a dire attempt to realizing it could have enormous adverse effects of the socio-environmental and economical life of the communities coming under its fire.

- Overoptimism and overcomplexity. In order to justify a project, sometimes costs and timelines are systematically underestimated and benefits systematically overestimated. Flyvbjerg argues that project managers competing for funding massage the data until they come under the limit of what is deemed affordable; stating the real cost, he writes, would make a project unpalatable. From the outset, such projects are on a fast track to failure. One useful reality check is to compare the project under consideration to similar projects that have already been completed. Known as “reference-class forecasting,” this process addresses confirmation bias by forcing decision makers to consider cases that don’t necessarily justify the preferred course of action. But, sadly, India does not have any avenues to a “reference-class forecasting”, for the country has hitherto not known anything on this scale.

- Poor execution. Having delivered an unrealistically low project budget, the temptation is to cut corners to maintain cost assumptions and protect the (typically slim) profit margins for the engineering and construction firms that have been contracted to deliver the project. Project execution, from design and planning through construction, is riddled with problems such as incomplete design, lack of clear scope, ill-advised shortcuts, and even mathematical errors in scheduling and risk assessment. In part, execution is poor because many projects are so complex that what might seem like routine issues can become major headaches. For example, if steel does not arrive at the job site on time, the delay can stall the entire project. Ditto if one of the specialty trades has a problem. Higher productivity will not compensate for these shortfalls because such delays tend to ripple through the entire project system. Another challenge is low productivity. While the manufacturing sector in India is languishing, raw materials for such mega-projects would always be hindered through supply lines, thus leading to either stalling of the projects, or an exponential cost escalation.

- Weakness in organizational design and capabilities. Many entities involved inbuilding megaprojects have an organizational setup in which the project director sits four or five levels down from the top leadership. The following structure is common:

Layer 1: Subcontractor to contractor

Layer 2: Contractors to construction manager or managing contractor

Layer 3: Construction manager to owner’s representative

Layer 4: Owner’s representative to project sponsor

Layer 5: Project sponsor to business executive

This is a problem because each layer will have a view on how time and costs can be compressed. For example, the first three layers are looking for more work and more money, while the later ones are looking to deliver on time and budget. Also, the authority to make final decisions is often remote from the action. Capabilities, or lack thereof, are another issue. Large projects are typically either sponsored by the government or by an entrepreneur with bold aspirations, where completion times are most often than not compromised.

Notes:

1 Micro Units Development & Refinance Agency Ltd. (MUDRA) is an institution set up by Government of India to provide funding to the non-corporate, non-farm sector income generating activities of micro and small enterprises whose credit needs are below ₹10 Lakh. Under the aegis of Pradhan Mantri MUDRA Yojana (PMMY), MUDRA has created three products i.e. ‘Shishu’, ‘Kishore’ and ‘Tarun’ as per the stage of growth and funding needs of the beneficiary micro unit. These schemes cover loan amounts as below:

- a Shishu: covering loans up to ₹50,000

- b Kishore: covering loans above ₹50,000 and up to ₹5,00,000

- c Tarun: covering loans above ₹5,00,000 and up to ₹10,00,000

All Non-Corporate Small Business Segment (NCSBS) comprising of proprietorship or partnership firms running as small manufacturing units, service sector units, shopkeepers, fruits/vegetable vendors, truck operators, food-service units, repair shops, machine operators, small industries, food processors and others in rural and urban areas, are eligible for assistance under Mudra. Bank branches would facilitate loans under Mudra scheme as per customer requirements. Loans under this scheme are collateral free loans.