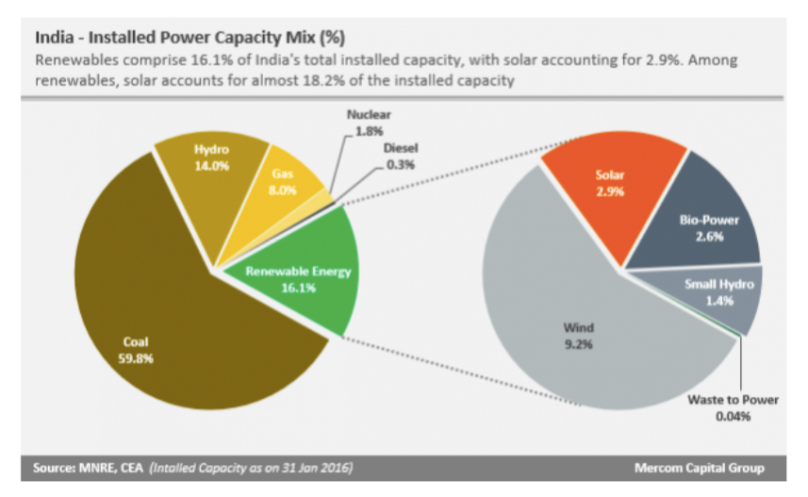

India is the seventh largest hydroelectric power generator in the world with a capacity approximating 45 GW comprising 13.5% of its total power generational capacity.1 Add to that a capacity of 4.4 GW of smaller hydroelectric power units, the total installed and generational capacity is furthered by 1.3%. The hydroelectric power potential is almost double of what is installed at the moment and stands at 84 GW at 60% of the load factor.2

The history of hydroelectric power generation in the country dates back to more than a century, when the British engineered the Sidrapong-1 in Darjeeling in West Bengal in 1897, which is still under operation. What really drives the efficiency of hydropower technology is design-oriented, but the advantages of longevity and cost of generation face compromises via energy mix, cases where India is well positioned to offset the advantages with reliance on fossil fuels. This has been witnessed from the decade of the 1960s, when hydropower accounted for close to 65% of total utility till the present times, where the proportion has fallen to 13.5%, thanks largely due to offsets created by thermal power. Although, the plummeting slide has been arrested of late due to environmental, social, economic and political factors, the other major reason for the reduction in hydropower portfolio has been attributed to consistently non-attainability of energy installation and generation targets.

The Government of India has taken many policy initiatives for sustainable hydropower development. In 2008, the Government came out with a hydro policy3 with an objective to achieve the implementation of these projects. Thereafter, the Centre and the states initiated hydropower projects through Public Private Partnerships (PPPs) to attract investors for the development of water resources in an environmentally-friendly manner and generate revenue while ensuring project viability. Despite the mechanism of PPP, many of these projects have had to struggle due to rehabilitation and resettlement concerns, problems associated with land acquisition, clearance and approval procedures, capability of developers, to name a few. These factors have indeed given the projects a troubled track record, but what is concerning are inherent risks associated with the hydro sector that makes investors averse to entering the fray. Inherent risks include geological surprises, calamities, environmental and forest-related concerns, and commercial risks, the last of which include high capital costs, and long payback period resulting from long gestation period culminating in a deterrence for the entry by the private players. Furthermore, hydropower projects are capital-intensive and thus financing them for long periods become a challenge. But, textbook project financing still continues to place private players as the fulcrum of financing hydro as well as renewables for the simple reason that these players seek commensurate returns with respect to risks involved in the sector. For these risks to effectuate into implementation, it is the onus of the Government to remove impediments along the way by either restoring investor faith in the sector or by creating an enabling environment.

The Financial Ecosystem

This section gives an overview of what financial players are involved in the hydropower sector.

The Indian hydropower financial sector could be zeroed in National Hydroelectric Power Corporation (NHPC) to begin with. NHPC, though a centrally-owned institution is not a typical financial intermediary, in that, it invests the funds that it raises directly. With an investment base of Rs. 3,87,180 million, the authorized share of this Mini Ratna Category-1 Government of India Enterprise is close to Rs. 1,50,000 million, which is exclusively held by the Government. Though, the mandate might seem to be wide-ranging, the portfolio of NHPC is actually quite modest, and the only noticeable expansion is the inclusion of development of wood and tidal power. NHPC pays only a nominal dividend on the equity capital which the Government holds, and receives a considerable grant support from the Ministry of Power. The main income is through sale of electricity and consultancy services, where the main clientele happens to be state electricity boards. NHPC has to put up 30% of the cost of every project which it develops s share capital. as it cannot develop this equity from the limited revenues of its own projects, the government needs to regularly increase its share capital. The other 70% of the cost is financed through debt. during the initial period of NHPC’s existence, this debt was provided by the Government. However, since the decade of the 1980s, NHPC started raising debts through commercial loans and bonds, both as private placements and public issues. The international source of funds for NHPC is through export credit agencies, and not through the multilateral development banks like the World Bank, or the Asian Development Bank.4

The other main agency involved in financing power is Power Finance Corporation, which unlike NHPC is a financial intermediary. The major part of PFC’s funds are raised through rupee-denominated bonds. Bonds issued by PFC enjoy the highest ratings in Indian and international markets and are on par with India’s sovereign rating. It borrows short-term and long-term from various banks and other financial institutions in addition to raising external commercial borrowings through private placement in the US market. PFC is the primary institution of the government of India for financing generation, transmission and distribution projects of the state electricity boards. Hydro projects up to 25 MW are financed by the Rural Electrification Corporation. Like the NHPC, PFC also provides consultancy services to its clientele. Like the international financial institutions, PFC has an attached conditionality clause to its loans, where the borrowers need to carry out Operational Financial Action Plans (OFAPs) in order to avail loans. The divide is clear between states that have undertaken power restructuring reforms getting loans at lower rates, while the states that have failed to undertake any such reforms have eventually lost out on PFC loans. The Government of India supports PFC’s resource mobilization in that PFC is attributed a large share of tax-free bonds on the Indian capital market. Rupee-bonds, loans from the Government and loans from Indian banks and other financial institutions form the domestic sources, while multilateral and bilateral agencies form the major sources of funds from international sources.5

Other major financial players happen to be Industrial Credit and Investment Corporation of India (ICICI), which extends rupee and foreign currency loans by raising capital internally and externally through concessional bonds6 from the Reserve Bank of India, or from syndicated loans as sourced from foreign commercial institutions, and bilateral credit lines from JBIC, KfW DFID; Industrial Development Bank of India (IDBI) extending loans and other assistance in rupees and foreign currencies by raising capital on both the domestic as well as international markets; and Infrastructure Development Finance Corporation (IDFC), which came into existence in 1997 with the aim to provide additional financing for private infrastructure projects. With Vishnuprayag in Uttarakhand and Srinagar in Uttar Pradesh, IDFC made forays into the hydroelectric sector sourcing its funds from bonds sold in the Indian capital market along with its share capital. IDFC, which has signed on to equatorial principles is probably India’s only financial institution to have any environmental policy. It has been quite disciplinarian in refusing loans to questionable projects, and thus has next to no non-performing assets in its portfolio.

Speaking of non-performing assets, the largest commercial bank in India, state Bank of India is facing quite a quagmire. Engaged in long-term project finance in the infrastructure sector, the bank is ignominious with the largest share of non-performing assets. The State Bank of India has played an advisory role in the possible merger of NHPC and National Thermal Power Corporation (NTPC), and in assessing the escrow capacities of state electricity boards for independent power producers (IPPs). As part of long-term infrastructure financing, the bank has ventured into hydropower directly, as well as extending funds for financial institutions and operators in the power sector. The major source of funding for the State Bank of India are its retail deposits, while bonds make up for long-term lending. Other sources include mobilizing foreign currency funds through international branch network. Its strong international position enables it to extend foreign currency loans directly from its foreign deposits, and to arrange international loan syndications. For example, the Bank provided loans to Maheshwar Hydro Electric Project through its Frankfurt branch.7

Hydropower lending is not just confined to commercial banks and development financial institutions, but even non-banking financial institutions. The leader in this category happens to be Life Insurance Corporation of India, or LIC in short. LIC has taken up bonds from and extended loans to state electricity boards and centrally-owned institutions like NTPC, NHPC, PFC, and the Power Grid Corporation. The issue of non-performing assets has plagued LIC, and the insurance company is almost on par with the State Bank of India with its distressed assets. Other non-banking financial companies like the General Insurance Corporation of India (GIC) and Unit Trust of India (UTI) are fast picking up their stakes in the power sector, and the reason for their lagging in comparison to LIC is because their funds do not have the same extended maturity as the funds of life insurer.

Since most of these institutions are Government owned, the role of private sector participation isn’t very much evident, but this should not be taken to mean that private sector involvement is compromised by the involvement of these public institutions. On the contrary, private-sector involvement is considered to be a catalyst for infrastructural development, though there are differing opinions about their role, or even if at all they should be invited. Notwithstanding the rationale behind their involvement, it is obligated we look at what promoted their invitation to the electricity sector in general and to hydropower in particular.

In 1991, the Government of India opened the hydropower development in the country to private participation and allowed 16 per cent return on equity (ROE)8 in 1992. The doors to private participation were further greased by the Electricity Act 20039, whose main objective was to promote competition for consumers to have the best possible price and quality of supply. The model to be adapted was similar to the World Bank model that was implemented in Odisha (then called Orissa) and thereafter picked up by other states. Called the “Single Buyer Mode”, the Act mandated that state electricity boards undertake unbundling of generation, transmission and distribution. The principal point in order to enhance generation, licensing had to be done away with completely excepting the need for techno-economic clearance for hydro projects. The Act was aimed at providing an investor friendly environment for potential developers in the power sector by removing administrative hurdles in the development of power projects by providing impetus to distribution reforms in India. Provisions like delicensing of thermal generation, open access and multiple licensing, and removal of surcharge for captive generation paved the basis for a competitive environment through private participation.

In 2008, Government came out with a policy called Power to All by 2012. Called the Hydro policy 2008, it encouraged private participation by giving incentives for accelerating the development of hydropower development in the country. Having failed in achieving its target of power to all by 2012, certain impeding factors like long gestation period, and capital intensive nature of the projects were held culpable. Private-sector implementation was augmented by the rise of Public Private Partnerships (PPPs), which are projects based on a contract or a concession agreement, between a government or statutory entity on the one side and a private sector company on the other side, for delivering an infrastructure service on payment of user charges. That PPP has been a policy game changer could be adduced from the fact that the Government is laying emphasis on it in order to resolve budgetary constraints, faster implementation of projects, reduced whole life costs, better risk allocation, improved quality of services, transfer of technology and project stability.10 though, how much of it is achieved and what are the likely hurdles in this model of development are subsequently discussed.

Private Engineering: Public Private Partnerships (PPPs) and Special Purpose Vehicles (SPVs)

India, undoubtedly has vast potential for renewables, but the execution is far from encouraging. One serious reason attributable to this has been the presence of strong coal-lobby in the country. Apart from this, energy economics plays its part, in that, any investment in hydropower development is decided by the cost of debt and the interest rate on capital. It is here that many of the private players who are majorly equity investors maintain focus on capital rates rather than on equity returns. Even if the operating portfolio of private investors is much larger thus facilitating easy accessibility to cheaper debt, unless the focus is on projects, which are profitable with adequate cash flow, renewable energy and infrastructure development in India would continue to face hurdles. For example, if a project is invested into with a debt-to-equity ratio of 70:30, with a typical interest rate of 14% and a repayment period of 8 years, an approximate 22% of the total project cost in the first year is outflow to service debt. It is well nigh difficult for projects to generate this kind of cash in the first year, simply owing to the fact that revenue assessment is not very critical. Bouncing off this critical gap are challenges that projects are more often than not over-advertised with under-estimation of revenue project costs and over-estimations of energy production potential leading to inconsistency in meeting the standard benchmark for haircuts. This is in close affinity with valuation expectations by developers where missing the woods for the trees is a high commonality due precisely to inadequate diligent processes.

But, does that mean this sector is riddled with detriments that cannot challenged off? It would be too far fetched to conclude this. Instead if the key issues like stringent adherence to budgets and timelines, reliable cash flow and accurate project valuations are held on to, these over-the-board-sounding-idealistic situations planned for contingencies, then most of the risks associated with financing and eventual implementation could be offset.

One of the two key instruments of private engineering happens to be Public Private Partnership (PPP). Public Private Partnerships are contractual arrangements between a public agency and a privately owned service provider. They are used to finance and operate projects that are considered important or desirable to the general public. Private agencies are incorporated because it has become increasingly apparent to both governments and donors that private enterprises are more cost-efficient and effective at delivering valuable products and services. The other instrument happens to be a Special Purpose Vehicle (SPV), which function as subsidiary entities for larger parent organizations and are typically used to finance new operations at favorable terms. The SPV can raise capital without carrying the debt or other liabilities of the parent organization even though the subsidiary is often operated by the same individuals and serves purposes that benefit the parent organization. SPVs are first and foremost an off-balance-sheet capital tool. This means that companies can change their overall asset/liabilities framework without having it show up in their primary financial statements. Many private partners in a PPP demand an SPV as part of the arrangement. This is especially true for very capital-intensive endeavors, such as an infrastructure project. The private company wants to limit its exposure to liabilities, so an SPV is created to absorb some of the risks. There isn’t a uniform operational role or legal design for the use of SPVs in a PPP; the particulars vary depending on the agreements of the actors and stakeholders in the project. However, every SPV needs to be created in accordance with the proper legal and accountancy rules in the jurisdiction. Most public projects rely on support from commercial banks or other financial institutions. Almost always, the SPV represents the financing wing and is used to attract funds from other lenders and investors. This protects the parent company and all financing parties from immediate counter-party risk. In the case of non-recourse financing, the lender’s only valid claims are limited to project assets in the case of default or non-completion. In turn, the SPV is not directly exposed to balance sheet issues with the parent or government agency. The government agency is often able to keep project debt and liabilities off its own balance sheet. This leaves more fiscal space for other public obligations. This can be especially important for governments that issue bonds because more fiscal space equates to higher bond credit ratings.11

Although SPVs and PPPs have come under tremendous criticism, which we would look into shortly, an example to show why even in the first place are these instruments required would help ease matters a bit. Consider a $1 billion collection of risky loan, obligations of borrowers who have promised to repay their loans at some point in future. Let us imagine them sitting on the balance sheet of some bank XYZ, but they equally well could be securities available on the market that the Bank’s traders want to purchase and repackage for a profit. No one knows whether the borrowers will repay, so a price is put on this uncertainty by the market, where thousands of investors mull over the choice of betting on these risky loans and the certainty of risk-free government bonds. To make them indifferent to the uncertainty these loans carry, potential investors require a bribe in the form of 20% discount at face value. If none of the loans default, investors stand a chance to earn a 25% return. A good deal for investors, but a bad one for the Bank, which does not want to sell the loans for a 20% discount and thereby report a loss.

Now imagine that instead of selling the loans at their market price of $800 million, the Bank sells them to an SPV that pays a face value of $1 billion. Their 20% loss just disappeared. Ain’t this a miracle? But, how? The SPV has to raise $1 billion in order to buy the loans from the Bank. Lenders in SPV will only want to put $800 million against such risky collateral. The shortfall of $200 million will have to be made up somehow. The Bank enters here under a different garb. It puts in $200 million as an equity investment so that the SPV has enough money now to buy the $1 billion of loans.

However, there is a catch here. Lenders no longer expect to receive $1 billion, or a 25% return in compensation for putting up the $800 million. SPV’s payout structure guarantees that the $200 million difference between face value and market value will be absorbed by the Bank, implying treating $800 million investment as virtually risk-free. Even though the Bank has to plough $200 million back into the SPV as a kind of hostage against the loans going bad, from Bank’s perspective, this might be better than selling the loans at an outright $200 million loss. This deal reconciles two opposing views, the first one being the market suspicion that those Bank assets are somehow toxic, and secondly the Bank’s faith that its loans will eventually pay something close to their face value. So, SPVs become a joint creation of equity owners and lenders, purely for the purpose of buying and owning assets, where the lenders advance cash to the SPV in return for bonds and IOUs, while equity holders are anointed managers to look after those assets. Assets, when parked safely within the SPV cannot be redeployed as collateral even in the midst of irresponsible buying spree.

So, if an SPV is such a robust engineering tool, why does it have to face up to criticisms? The answer to this quandary lies in architecture, the architectural setup of SPVs drawing on the Indian context. SPVs are invested with responsibilities to plan, appraise, approve, releasing funds, implement, and evaluate development projects within the ambit of financing renewable projects, including hydropower. According to the Union Government, every SPV will be headed by a full-time CEO, and will have nomination from the central and state government in addition to members from the elected Urban Local Bodies (ULBs) on its Board. Who the CEO isn’t clearly defined, but if speculation is to be believed in concomitance with PPP, these might be from the corporate world. Another justification lending credence to this possibility is the proclivity of the Government to go in for Public-Private Partnerships (PPPs). The states and ULBs would ensure that a substantial and a dedicated revenue stream is made available to the SPV. Once this is accomplished, the SPV would have to become self-sustainable by inculcating practices of its own credit worthiness, which would be realized by its mechanisms of raising resources from the market. It needs to re-emphasized here that the role of the Union Government as far as allocation is concerned is in the form of a tied grant through creating infrastructure for the larger benefit of the people. This role, though lacks clarity, unless juxtaposed with the agenda that the Central Government has set out to achieve, which is through PPPs, Joint Ventures (JVs) subsidiaries and turnkey contracts.

If one were to look at the architecture of SPV holdings, things get a bit muddled in that not only is the SPV a limited company registered under the Companies Act 201312, the promotion of SPV would lie chiefly with the state/union territory and elected ULB on a 50:50 equity holding. The state/UT and ULB have full onus to call upon private players as part of the equity, but with the stringent condition that the share of state/UT and ULB would always remain equal and upon addition be in majority of 50%.13 So, with permutations and combinations, it is deduced that the maximum share a private player can have will be 48% with the state/UT and ULB having 26% each. Initially, to ensure a minimum capital base for the SPV, the paid up capital of the SPV should be with an option to increase it to the full amount of the first installment provided by the Government of India. This paragraph commenced saying the finances are muddled, but on the contrary this arrangement looks pretty logical, right? There is more than meets the eye here, since a major component is the equity shareholding, and from here on things begin to get complex. This is also the stage where SPV gets down to fulfilling its responsibilities and where the role of elected representatives of the people, either at the state/UT level or at the ULB level appears to get hazy. Why is this so? The Board of the SPV, despite having these elected representatives has in no certain ways any clarity on the decisions of those represented making a strong mark when the SPV gets to apply its responsibilities. SPVs, now armed with finances can take on board consultative expertise from the market, thus taking on the role befitting their installation in the first place, i.e. going along the privatization of services in tune with the market-oriented neoliberal policies in new clothes sewn with tax exemptions, duties and stringent labour laws in bringing forth the most dangerous aspect, viz. privatized governance.

In India, private engineering is plugged in with Government initiatives through a host of measures by the latter in creating fecund grounds furthering efficiency and faster execution. Responsibilities are no more split between Ministry of Power, Ministry of Coal and Ministry of New and Renewable Energy, for hitherto it was difficult managing projects under departments working in silos at the central level. Ever since the present ruling dispensation of National Democratic Alliance (NDA) stressed on making hydropower a cardinal component in the energy mix for the country, the Government of India has undertaken a number of initiatives in the recent past, supported by various policy-level changes to promote hydropower development and facilitate investment in the sector. As a part of these initiatives, the government has increased financial allocation, along with other non-financial support, and is also in the process of establishing a dedicated hydropower development fund14 to improve the investment attractiveness of the sector. Other than that, the government could use the clean energy fund to provide loans to hydro projects at a lower rate of interest. On a smaller scale, the Indian Renewable energy Development Agency (IREDA), National Clan Energy Fund (NCEF) has already launched a refinancing scheme by providing loans at 2% for the revival of operational small hydro-projects (SHP) and biomass projects which have been affected by low tariffs, low plant load factor (PLF) levels, or force majeure conditions.15 Government’s promise to offer long-term finance to infrastructure projects, and meet the country’s target of generating 15% of its energy from renewable sources affirms its commitment to providing financial and administrative assistance to hydropower generation, the economic viability of which would be determined by investors and developers. It needs to be noted that as of now, not all of hydropower is considered to be renewable, but the government is mulling over the fact that all of hydropower needs to be categorized as such. At present, hydropower projects below 25 MW are considered renewables, and comes under the purview of the Ministry of New and Renewable Energy. Large hydro is with the Ministry of Power, as is National Hydro Power Corporation (NHPC). If all of hydropower is categorized under renewable energy, it would facilitate the Government to meet its Intended Nationally Determined Contributions (INDC) targets, as committed in the Paris Climate-Change summit 2016. The Indian government had committed to 40% of its total energy generation from renewable sources. Solar and wind power cumulatively contribute 15% to the energy mix. Adding hydro would take the total close to 30%. The current generation capacity of hydro is 44,189 MW out of the total installed capacity of 314,000 MW. According to Piyush Goyal, Former Minister for Power, Coal, Mines and Renewable Energy, getting to consider all of hydropower as renewable would ensure coverage under RPO16 and qualify for dispatch priority. Recognising hydropower as renewable might, however, not mean that its purchase will be included in the renewable purchase obligation (RPO) of distribution companies. Currently, the government guidelines for the long-term RPO trajectory keep hydropower out of the calculation of total energy consumption, and thus for any change to be effectuated, the Government would have to discuss the details with the stakeholders, including segment regulators. 17 18

Considering an energy elasticity of 0.819, India is projected to require around 7% annual growth in electricity supply to sustain a GDP growth of around 8.5% p.a. over the next few years. This requires tapping all potential sources to address the deficit and meet the demand growth for accelerating economic development while taking into account considerations of long-term sustainability, environmental and social aspects. Though reservoir-based hydropower projects have come under criticism due to CO2 and methane emissions beyond acceptable limits, most hydro-rich countries have followed an integrated full life-cycle approach for the assessment of the benefits and impacts to ensure sustainability20. India is no different in this regard.

Financing Power: Generic Trends

This section focuses on the generic trends that involve financing power in the country, and many of the trends overlap across sectors, in that these are true for thermal, hydro and renewable energy generation. Moreover, the section, though slightly technical in nature, is interspersed with what may eventually count as accommodating structure for procurement of funds and thus departs from the norm in that it looks to policy and regulatory mechanisms in place and those that are aspirational or in the form of recommendations. Moreover, the section also delves into what is probably the hardest challenge facing the Indian Banking sector at the moment, viz. Non-Performing Assets (NPAs). There are documents and reports by the score that highlight how infrastructure development, including the power sector in India is riddled with NPAs.21 As a caveat, one maybe at a loss in linking this section with hydropower in particular due to its genericity, but one needs to comprehend the financial complexities from policy and regulatory points of view in order to appreciate the fuller magnitude of financing hydropower in particular and power sector in general.

Banks and Infrastructure Finance Companies (IFCs) are the predominant sources of financing of power sector in India. Balance sheet size of many Indian banks and IFCs are small vis-à-vis many global banks. Credit exposure limits of banks and IFCs towards power sector exposure is close to being breached. Any future exposure seems to be severely constrained by balance sheet size, their incremental credit growth and lack of incentives to lend to power sector. The desirability and sustainability of sectoral exposure norms of the banks in the future may be examined in view of the massive exposure of the banks and projected fund requirements for the power sector. Further, any downgrade in the credit rating of power sector borrowers would adversely impact the ability of the major Non Banking Financial Companies (NBFCs) viz. Power Finance Corporation (PFC) and National Hydro Power Corporation (NHPC) to raise large quantum of funds at a competitive rate from domestic as well as international capital markets. In such a scenario, the sources of funds available for power sector projects are expected to be further constrained.

The capital intensive nature of power projects requires raising debt for longer tenure (more than 15 years) which can be supported by life of the Power Project (around 25 years). However, there is wide disparity between the maturity profiles of assets and liabilities of banks exposing them to serious Asset Liability Maturity mismatch (ALM). Accordingly, the longest term of debt available from any bank or financial institution is for 15 years (door-to-door) which could create mismatch in cash flow of the Power project and may affect the debt servicing. Options like refinancing are explored to make funds available for the power project for a long tenor. Though maturity profiles of funds from insurance sector and pension funds are more suited to long gestation power projects, only a minuscule portion is deployed in power sector. At this stage, it becomes appropriate to talk of how and why pension funds are not really the funds to run after when it comes to financing Hydropower in the country. That these funds are not the de facto choice would be statement made in a hurry, for the government could in time switch financing instrumental gears to cater to investments in hydropower, provided these are amalgamated with Green bonds. Internationally, the Green bonds base is up-north of $82 billion, whereas in India, the Green bonds are minuscule, but all slated for an exponential growth. Banks like Yes Bank and World Bank have launched green bonds. Green Bonds as a debt instrument by an entity raising funds ‘earmarked’ for use towards financing ‘green’ projects, assets, and business activities with environmental benefits. It attracts new class investor base – insurance funds, pension funds, sovereign wealth funds apart from the traditional investors. It helps in enhancing an issuer’s reputation illustrates green credentials of the issuer and demonstrates commitment towards the development and sustainability of the environment. The caution is that green bonds come with currency risk. However, if one raises green masala bonds, one will not have the risk of forex. To have the need for appropriating fiscal incentives in order to explore the ways to channelize savings, new debt instruments and sources of funds viz. Infrastructure Debt Fund, Clean Energy Funds etc. are identified for the purpose of infrastructure financing.

When it comes to cost of funds, cost of Rupee funding is high as compared to foreign currency funding due to currency fluctuations in the form of appreciation and depreciation. In a competitive bidding scenario, higher cost of borrowing could adversely affect the profitability and debt servicing of loan. External Commercial Borrowings (ECBs) for power projects is not well suited due to issues relating to tenor, hedging costs, exposure to foreign exchange risks etc. Project financing by multilateral agencies (World Bank, Asian Development Bank) has been low due to various issues.22 While bond offerings are a lower cost option to raise funds vis-à-vis syndicated loans, corporate bond market for project financing is virtually absent in India. Innumerable committees have opined on the reasons for the relative underdevelopment of India’s corporate bond market. However, despite several recommendations being implemented, there is still anaemic activity in existing corporate bonds, and anaemic issuance of new corporate bonds in relative terms. In addition, it appears that debt to equity ratios of Indian corporates have been falling steadily since the late 1990s, potentially a symptom of relative reductions in activity in the corporate debt market. Theoretically the presence of corporate bonds would provide an important alternative source of funding for corporations, which will enable them to optimize capital structure in an environment of friction. Such a market should enable additional cash to fund operations or long-term expansion plans without diluting corporate control. The government should also welcome the development of the corporate bond market because it would spur corporate activity and thus economic growth. Finally, investors such as pension funds and insurance companies should welcome corporate bonds as an additional set of instruments in which to invest, providing, in theory, a better overall risk to reward trade-off since there would be more opportunities for diversification. But, despite all these positives, the corporate bond market in the country is anemic. One important fact might hold the clue to explaining the lack of growth of this market. That is the huge pile of corporate debt that is currently being held in the form of loans, especially by state-owned banks. This massive inventory of loans generates significant incentives for three parties – banks, corporations and the government – to delay or inhibit the development of a significant corporate bond market. It goes without saying that large corporations with significant levels of unsustainable debt have no incentive to issue increased levels of debt, and indeed, have significant incentive to ensure the creation and perpetuation of information asymmetries that will inhibit liquidity in the market for their debt. So, the problem is not merely a problem of demand – from banks, but, also extends to debt supply. From the government’s point of view, there is a trade-off. In the short run, enabling a vibrant corporate bond market will result in significant losses to the banking sector, especially for nationalized banks, which are significantly exposed to bad corporate loans. This is because better price discovery will reveal the full extent of the problem of non-performing assets resulting from exposure to over-leveraged corporates. It is also the case that there may be more corporate failures if the full scale of the bad loans problem is revealed to the world. But, it must also be remarked that the credit rating of the power projects being set up under Special Purpose Vehicle (SPV) structure is generally lower than investment criterion of bond investors and thus there is a need for credit enhancement products.

Creation of specialized long-term debt funds to cater to the needs of the infrastructure sector; a regulatory and tax environment that is suitable for attracting investments is the key for channelizing long-term funds into infrastructure development. Reserve Bank of India (RBI) may look into the feasibility of not treating investments by banks in such close-ended debt funds as capital market exposure. Insurance and Regulatory Development Authority of India (IRDA) may consider including investment in Securities and Exchange Board of India (Sebi) registered debt funds as approved investments for insurance companies. Insurance Companies, Financial Institutions are encouraged/provided incentives to invest in longer dated securities to evolve an optimal debt structure to minimize the cost of debt servicing. This would ensure lowest tariff structure and maximum financial viability. Option of a moratorium for an initial 2 to 5 years may also reduce tariff structure during the initial years. One of the most serious contenders for acquiring funds and one that has been extensively experimented with is the Viability Gap Funding (VGF). The power projects that are listed under in generation or transmission and distribution schemes in remote areas like North-eastern region, J&K etc and other difficult terrains need financial support in the form of a viability gap for the high initial cost of power which is difficult to be absorbed in the initial period of operation. A scheme may be implemented in the remote areas as a viability gap fund23 either in the form of subsidy or on the lines of hydropower development fund, a loan which finances the deferred component of the power tariff of the first five years and recovers its money during 11th to 15th year of the operation may be introduced. Any extra financing cost incurred on such viability gap financing should also be permitted as a pass through in the tariff by regulators.

Green Bonds

Shifting terrain here, it is obligatory to talk of green bonds and how they could be the next ‘big’ thing in financing. Green bonds are like other bonds with the key difference being the former are specifically used for ‘green’ projects that are environmentally friendly. These bonds could help reduce the cost of capital if there are open door policies aimed towards attracting foreign investment, and especially so, when Foreign Direct Investment policies in India are getting more and more market friendly. The history of ‘green’ bonds could be dated back to 2007, when the European Investment Bank and the World Bank launched these bonds. Subsequently, 2013 witnessed corporation participation leading to its overall growth. In India, Yes Bank became the first bank to issue these bonds worth Rs. 1000 crore in 2015.

So, what of Sebi24 and any of rules and regulations mandating additional information about these bonds? For designating an issue of a corporation bond as a ‘green’ bond, an issue apart from complying with the issue and listing of debt securities regulations, the corporation would have to disclose additional information in the offer document such as use of proceeds. Sebi’s board had considered and approval a proposal for issuance and listing of green bonds way back in January 2016 to help meet the huge financing requirements worth USD 2.5 trillion for climate change actions in India by 2030. It is to be noted that ‘green’ bonds can be key to help meet an ambitious target India has of building 175 gigawatt of renewable energy capacity by 2022, which will require a massive estimated funding of $200 billion. Hydropower has a significant role to play in achieving the goals of the Paris Agreement.25 Supporting the growth of the green bonds market is an important step towards aligning emission reduction targets with appropriate market signals and incentives.26 One example of Green bonds being used to finance hydropower in India is the Rampur Hydropower Project, across River Satluj in Simla and Kullu districts of Himachal Pradesh. This 412 MW installed capacity project has been financed on a 70:30 debt equity ratio basis, and is backed by a US$ 400 million by the World Bank.27

Shifting terrain once more, let us now focus on policy-wide measures that feed into renewables.

Policy-wide Measures for Take-out Financing

The Reserve Bank of India (RBI) has stipulated guidelines for Take-out Financing through External Commercial Borrowings (ECB) Policy.28 The guidelines stipulate that the corporate developing the infrastructure project including Power project should have a tripartite agreement with domestic banks and overseas recognized lenders for either a conditional or unconditional take-out of the loan within three years of the scheduled Commercial Operation Date (COD). The scheduled date of occurrence of the take-out should be clearly mentioned in the agreement. However, it is felt that the market conditions cannot exactly be anticipated at the time of signing of document and any adverse movement in ECB markets could nullify the interest rate benefit that could have accrued to the project. Hence, it is suggested that tripartite agreement be executed closer to project COD and instead of scheduled date of occurrence of the take-out event, a window of 6 or 12 months could be mentioned within which the take-out event should occur.

Further, the guidelines stipulate that the loan should have a minimum average maturity period of seven years. However, an ECB of average maturity period of seven years would entail a repayment profile involving door-to-door tenors29 of eight to ten years with back-ended repayments. It is likely that ECB with such a repayment profile may not be available in the financial markets. Further, the costs involved in hedging foreign currency risks associated with such a repayment profile could be prohibitively high. Hence it is suggested that the minimum average maturity period stipulated should be aligned to maturity profiles of ECB above USD 20 million and up to USD 500 million i.e. minimum average maturity of five years as stipulated in RBI Master Circular No.9 /2011-12 dated July 01, 2011.30 RBI exposure norms applicable to IFCs allow separate exposure ceilings for lending and investment. Further, there is also a consolidated cap for both lending & investment taken together. In project funding, the IFCs are mainly funding the debt portion and funding of equity is very nominal.31 Therefore, the consolidated ceiling as per RBI norms may be allowed as overall exposure limit with a sub-limit for investment instead of having separate sub-limits for lending and investment. This will leverage the utilization of un-utilized exposures against investment. It is well justified since lending is less risky as compared to equity investment. This will provide additional lending exposure of 5% of owned funds in case of a single entity and 10% of owned funds in case of single group of companies, as per existing RBI norms. RBI Exposure ceilings for IFCs are linked to ‘owned funds’ while RBI exposure norms as applicable to Banks & FIs (Financial Institutions, but also Financial Intermediaries) allow exposure linkage with the total regulatory capital i.e. ‘capital funds’ (Tier I & Tier II capital). Exposure ceilings for IFCs may also be linked to capital funds on the lines of RBI norms applicable to Banks. It will enable to use the Tier II capitals like Reserves for bad and doubtful debt created under Income Tax Act, 196132, for exposures.

RBI norms provide for 100% provisioning of unsecured portion in case of loan becoming ‘doubtful’ asset. Sizable loans of Government IFCs like PFC and NHPC are guaranteed by State Governments and not by charge on assets. On such loans, 100% provisioning in first year of becoming doubtful would be very harsh and can have serious implication on the credit rating of IFC. Therefore, for the purpose of provisioning, the loans with State/Central Government guarantee or with undertaking from State Government for deduction from Central Plan Allocation or Direct loan to Government Department may be treated as secured. As per RBI norms, the provisioning for Non-Performing Assets (NPAs) is required to be made borrower-wise and not loan-wise if there is more than one loan facility to one borrower. Since Government owned IFC’s exposure to a single State sector borrower is quite high, it would not be feasible to provide for NPA on the total loans of the borrowers in case of default in respect of one loan. Further, the State/Central sector borrowers in power sector are limited in numbers and have multi-location and multiple projects. Accordingly, default in any loan in respect of one of its project does not reflect on the repaying capacity of the State/Central sector borrowers. A single loan default may trigger huge provisioning for all other good loans of that borrower. This may distort the profitability position. Therefore, provisioning for NPAs in case of State/Central sector borrowers may be made loan-wise. In case of consortium financing, if separate asset classification norms are followed by IFCs as compared to other consortium lenders which are generally banking institutions; the asset classification for the same project loan could differ amongst the consortium lenders leading to issues for further disbursement etc.

Prudential Norms relating to requirement of capital adequacy are not applicable to Government owned IFCs. However, on the other side, it has been prescribed as an eligibility requirement for an Infrastructure Finance Company (IFC) being 15% (with minimum 10% of Tier I capital). Accordingly, Government owned IFCs are also required to maintain the prescribed Capital Adequacy Ratio.33 Considering the better comfort available in case of Government owned IFCs, it is felt that RBI may consider stipulating relaxed CAR requirement for Government owned IFCs. It will help such Government owned IFCs in better leveraging. RBI prudential norms applicable to IFCs require 100% risk weight for lending to all types of borrowers. However, it is felt that risk weight should be linked to credit rating of the borrowers. On this premise, a 20% risk weight may be assigned for IFC’s lending to AAA rated companies. Similarly, in case of loans secured by the Government guarantee and direct lending to Government, the IFCs may also assign risk weight in line with the norms applicable to banks. Accordingly, Central Government and State Government guaranteed claims of the IFC’s may attract ‘zero’ and 20% risk weight respectively. Further their direct loan/credit/overdraft exposure to the State Governments, claims on central government will attract ‘zero’ risk weight.

As per extant ECB Policy, the IFCs are permitted to avail of ECBs (including outstanding ECBs) up to 50% of their owned funds under the automatic route, subject to their compliance with prudential guidelines. This limit is subject to other aspects of ECB Policy including USD 500 million limit per company per financial year. These limits/ceilings are presently applicable to all IFCs whether in State/Central or Private Sector. Government owned IFCs are mainly catering to the funding needs of a single sector, like in Power sector where the funding requirements for each of the power project is huge. These Government owned IFCs are already within the ambit of various supervisory regulations, statutory audit, CAG audit, etc. It, is, therefore, felt that the ceiling of USD 500 million may be increased to USD 1 billion per company per financial year for Government owned IFCs. Further, the ceiling for eligibility of ECB may also be increased to 100% of owned funds under automatic route for Government owned IFCs to enable them to raise timely funds at competitive rates from foreign markets. Thus, these measures will ensure Government owned NBFC-IFCs to raise timely funds at competitive rates thereby making low cost funds available for development of the infrastructure in India.

Enabling and Disabling Environment for Hydropower(Conclusion)

Though some bottlenecks remain. With the present power scenario and major policy initiatives to increase renewable capacity (mainly solar and wind), it is becoming difficult to sell hydropower. There is reluctance on the part of distribution utilities to enter into long term Power Purchase Agreements (PPAs). The government should declare all Hydropower Projects, regardless of the capacity, as “Renewables”, particularly, the Run of the River ROR (with or without diurnal pondage) projects. Presently Ministry of Power gives pooled quota of electricity from Central Public Sector Undertakings to various states. Ministry of Power should include Hydropower projects in the pooled quota for enabling faster PPAs. There should be separate Hydropower Purchase Obligation (HPO), too. The other bottleneck remains to be addressed is Tariff. Tariffs from hydropower projects are higher in the initial years as compared to other sources due to lack of incentives like tax concessions, financing cost and construction of projects in remote areas with inadequate infrastructure. Mega Power benefits were terminated in 2012. Major benefits associated with the Mega Power status were custom duty exemption on import of capital equipment and excise duty exemption. Mega Power benefits should be reintroduced. Since taxes constitute 15-25 per cent of project cost, it is still too early to fathom the import of Goods and Services Tax (GST) on the sector to contour its full consequences. Long term funding for hydropower project development is essential and needs to be directed through a policy. Creation of sub sectoral limit for lending to hydropower projects on priority basis by banks is the need of the hour to revive hydropower sector in India. The Banks should be advised to earmark at least 40 per cent of the total lending to power sector dedicated only for hydropower projects. Since Hydro Electric Projects are prone to various risks and uncertainties, the Return on Equity should not be decreased, except in cases of delays on account of developer. Service tax exemption to services used for Hydro Power Projects shall also lead to reduction of tariff. To reduce the weighted average cost of capital for competitive tariff, it is suggested that Debt to Equity ratio should be kept flexible say 80:10:10 with mandatory incurrence of equity portion minimum of 50 per cent before any disbursement. Funding could be 80 per cent Debt and 10 per cent Subordinate Debt. This could, by way of promoting hydropower as a renewable source of energy be considered as a positive for India, but what really has not been accounted for is socio-environmental and economic consequences, which would in many a cases be irreparable. The third crucial aspect that needs to be addressed is financing, or rather hurdles to financing. Due to long construction period of hydro projects, interest on loan plays a very critical role in increasing project cost. Also, during operation period, higher interest on outstanding loan leads to higher yearly tariff. Non-availability of longer tenure loan necessitates higher provision for depreciation so as to generate resources required to meet repayment obligations. Benefits under section 10(23)g of IT Act, 1961 to Hydro Power Projects, which allowed for the exemption of tax on the interest income earned by the Financial Institutions from Infrastructure projects, were withdrawn and is not available with respect to infrastructure projects. As per the current regulations, State Government is to be provided 12 per cent free power as royalty from any Hydro Power Project to be developed in the State. This provision of free power to the State affects the financial viability of the project severely. Due to the very challenging and difficult logistics, cost of the Project in any case is high and provision of high royalty in terms of free power, makes the project even more costlier and tariff becomes almost unsustainable. A review and revision of the financing policies for hydro projects are required with a view to provide longer tenure debt to hydro sector (say 25-30 years). Subsidy on the rate of interest on debt during the construction period of the projects should be introduced to reduce the Interest During Construction (IDC). Softer interest rates should be extended to large Hydro Plants. Tax Holiday under Section 80I (A) of the Income Tax Act, 1956 should be made applicable for 15 years for all Hydro Power Projects including under implementation projects. Hydropower projects are subjected to various types of risks like hydrological risk, power evacuation risk, geological surprises, construction risk, connectivity issues due to remote locations, extreme terrain etc. But after the commissioning of the Hydro-Electricity Plant, the majority of the risks are mitigated. The Financial Institutions, along with consortium lenders should be advised to extend the interest rebate on long term loans post commissioning of the project.

It is not just financing alone that is driven by development banks, but even building policy and regulatory mechanisms that are taken on board for creating an enabling environment to realize the true potential of hydropower leading to a spur in investments. This is mostly done with an emphasis on treating hydropower potential as a solution to long-term energy goals. The private arm of the World Bank, International Finance Corporation (IFC) has classified a new source of finance termed “Infraventures”, also known as the IFC Global Infrastructure Project Development Fund, is a $150 million global infrastructure fund that aims to develop a “bankable” pipeline of public-private partnerships and private projects for infrastructure. This fund and others are catalyzing the development of big hydropower by decreasing the initial financial barriers to investment and decreasing the financial risks so that the project is attractive to the private sector. For IFC Infraventures, the IFC then gets an equity stake in return. It is not unreasonable to claim that such approaches are criticized by Civil Society Actors34 citing serious implications for transparency, accountability and governance.

With the mushrooming of new development banks like BRICS Bank, Asia Infrastructure Investment Bank, consideration for financing of hydropower projects has got a fillip in complementing the agenda of the already existing development banks like the World Bank and the Asian development Bank. But, the main funding spigot in the sector has changed course in India. Even though the multilateral development banks and a host of bilateral financing arrangements, be they wrought by EXIMs or bilaterally negotiated, have the necessary influence to bring to realization projects of scales varying from big hydro to run-of-the-river schemes, their actual influx by way of funds has been reduced to a mere chunk compromised by national financial institutions, either banking or non-banking.

The majority of the funds are pumped in by these national institutions, even if their drive is monitored through equity investments by international financial institutions. Critics of the arrangement often point out to such a huge share as leading to stresses on the banking system eventually paving the way for NPAs. Experience has shown that the impacts of hydropower can be devastating, resulting in physical and economic displacement, the disenfranchisement of indigenous people’s rights, and the destruction of fragile ecosystems. Despite the historically significant impacts of hydropower, the information provided to affected communities and to the general public appears to be woefully inadequate.35 As the authors36 seem to vociferously declare that the all too common adverse consequences of hydro projects do not seem sufficient to prompt a modification on development banks’ investment priorities. The narrative that paints hydropower as source of clean and cheap energy continues to drive banks’ priorities while sweeping under the rug the unacceptable price paid by marginalized members of society.

1) Government of India, Ministry of Power, Central Electricity Authority. Power Sector 2017 <http://www.cea.nic.in/reports/monthly/executivesummary/2017/exe_summary-04.pdf>

2) Government of India, Ministry of Power, Central Electricity Authority. Hydro Planning and Investigation Reports. Page last updated: Mon Feb 13 2017 <http://www.cea.nic.in/monthlyhpi.html>

3) Government of India, Ministry of Power. Hydro Power Policy 2008 <http://www.ielrc.org/con- tent/e0820.pdf>

4) Bosshard, P. Power Finance: Financial Institutions In India’s Hydropower Sector. pp 36-38. January 2002. <http://www.sandrp.in/hydropower/Power_Finance.pdf>

5) Bosshard, P. Power Finance: Financial Institutions In India’s Hydropower Sector. pp 43-48. January 2002. <http://www.sandrp.in/hydropower/Power_Finance.pdf>

6) A concession is a selling group’s compensation in a stock or bond underwriting agreement. The amount of compensation is based on the underwriting spread, or the difference between what the public pays for the securities and what the issuing company receives from the sale.

7) Bosshard, P. Power Finance: Financial Institutions In India’s Hydropower Sector. p 66. January 2002. <http://www.sandrp.in/hydropower/Power_Finance.pdf>

8) Return on Equity is a measure of profitability that calculates how many dollars of profit a company generates with each dollar of shareholders’ equity. Also referred to as return on net worth, it is formulaically ROE = (Net Income)/(Shareholders’ Equity).

9) Ministry of Law and Justice, Legislative Department. The Electricity Act, 2003. 2 Jun 2003. <http://www.cercind.gov.in/Act-with-amendment.pdf>

10) Ullah, A. Public Private Partnership in Hydro-Power Development of India: Prospects and Challenges. In Journal of Business Management & Social Sciences Research (JBM&SSR). volume 4, No. 2, February 2015.

11) Investopedia. What role do SPVs / SPEs play in public-private partnerships? Mar 09 2015 <http://www.investopedia.com/ask/answers/030915/what-role-do-spvs-spes-play-publicprivate-partnerships.asp>

12) Government of India, Ministry of Corporate Affairs. The Companies Act, 2013. <http://ebook.mca.gov.in/default.aspx>

13) Government of India, Ministry of Housing and Urban Affairs. Smart Cities Mission. 18 Jul 2017. <http://smartcities.gov.in/content/innerpage/spvs.php>

14) PricewaterhouseCoopers & ASSOCHAM India. Hydropower @ Crossroads. pp 7 and 14. 2016 <https://www.pwc.in/assets/pdfs/publications/2016/hydropower-at-crossroads-pwc-assocham-report.pdf>

15) Indian Renewable Energy Development Agency Ltd. IREDA-NCEF Refinance Scheme for Scheduled Commercial Banks/FIs for Refinancing of their outstanding loans against Biomass Power & SHP Projects. 31 JUL 2017 <http://www.ireda.gov.in/writereaddata/Revised%20-%20IREDA%20NCEF%20Refinance%20Scheme.pdf>

16) Renewable Purchase Obligation refers to the obligation imposed by law on some entities to either buy electricity generated by specified ‘green’ sources, or buy, in lieu of that, ‘renewable energy certificates (RECs)’ from the market. The ‘obligated entities’ are mostly electricity distribution companies and large consumers of power. RECs are issued to companies that produce green power, who opt not to sell it at a preferable tariff to distribution companies.

17) Jai, S. Uncharted waters for hydropower’s renewable energy status. Business Standard. 24 Mar 2017 <http://www.business-standard.com/article/companies/uncharted-waters-for-hydropower-s-re-status-117032301145_1.html>

18) Small hydro currently enjoys a slew of concessions such as tax benefits and easier environment and water clearance. To promote it as a RE source, the Centre also offers subsidy support of Rs 5 crore per MW and/or Rs 20 crore per project. To replicate these subsidies for a large project would be very heavy on government finances. Also, this move to make large hydro as renewable only benefits the country, not the sector. The sector would have to wait for the new GST (goods and services tax) regime to kick in, to know what concessions are in store for them. The earlier 10-year tax holiday for power projects has ceased to exist. Excise, Customs and like duties would be decided after the GST is notified for the sector. The Government could be looking at removing the whole subsidy mechanism for the sector, like it did in solar and wind power. So, the first target (of its proposed move) is obviously to meet the INDC and the other could be to reform the sector by linking it to market forces. The subsidy in hydro is for loan repayment and that can only happen when a project is operational. Hydro faces operational issues, regulatory hurdles and local issues. These need to be addressed. A speedy approval mechanism would entail growth of the sector.

19) Mohanty, A. & Chaturvedi, D. Relationship between Electricity Energy Consumption and GDP: Evidence from India. In International Journal of Economics and Finance; Vol. 7, No. 2; 2015. pp 186-202.

20) PWC & FICCI. Hydropower in India: Key enablers for a better tomorrow. 2014 <http://www.pwc.in/assets/pdfs/publications/2014/hydropower-in-india-key-enablers-for-better-tomorrow.pdf>

21) A Non-Performing Asset (NPA) is defined as a a credit facility in respect of which the interest and/or installment of Bond finance principal has remained ‘past due’ for a specified period of time. NPA is used by financial institutions that refer to loans that are in jeopardy of default. In the Indian context: You may note that for a bank, the loans given by the bank is considered as its assets. So if the principle or the interest or both the components of a loan is not being serviced to the lender (bank), then it would be considered as a Non-Performing Asset (NPA). Any asset which stops giving returns to its investors for a specified period of time is known as Non-Performing Asset (NPA). Generally, that specified period of time is 90 days in most of the countries and across the various lending institutions. However, it is not a thumb rule and it may vary with the terms and conditions agreed upon by the financial institution and the borrower. Has the hydropower sector been impacted? In March 2017, India Ratings Downgraded Indira Priyadarshini Hydro Power’s Loans to ‘IND D’. The downgrade reflects the instances of delays of up to 90 days in servicing of debt obligations by IPHPPL during the three months ended February 2017, due to tight liquidity position. IPHPPL is sponsored by the Ind Barath group of companies, which is mainly engaged in the power development business. The company is setting up a 4.8MW run-of-the-river hydel power plant on Manuni khad (tributary of Beas) in Kangra District, Himachal Pradesh. The power plant is yet to be commissioned. Bank facilities have low complexity levels which reflect that the relationship between the inherent risk factors and intrinsic return characteristics is straightforward.

22) The transition to private participation in infrastructure has not yet settled; consequently, the financing environment for developing-country infrastructure is not clearly defined. In many developing countries, the agenda of market liberalization, regulatory reform, and the restructuring of state-owned monopoly utilities remains unfinished. Furthermore, given the characteristics of certain infrastructure industries, including the huge sunk costs involved, elements of natural mono- poly, and their political saliency, there remains a strong rationale for state intervention, even in cases where privatization has been completed. Also, investors must factor in ongoing transformations of the global infrastructure industry, such as how to accurately price and gauge demand for new products resulting from rapid technological change. Together with a series of recent financial crises, these developments have taken their toll, presenting a hierarchy of risks at the industry, country, and project levels. Those risks raise the cost of capital and make investors and creditors averse to long-term investments in developing- country infrastructure.

23) According to New Hydropower Policy 2017, which is in the pipeline, there would be provisions with viability gap funding for projects, compulsory hydropower purchase obligations for distribution companies and a set of good practices that states would have to follow. The policy being prepared by the power ministry will have provisions for viability gap funding, which will help in meeting the shortfall in project costs and reducing hydroelectricity tariffs for consumers. Hydropower is expensive and in some cases more than double the cost of power from coal-based thermal plants. Compulsory hydropower purchase from large projects will either be made part of the existing renewable power purchase obligation of distribution companies or a separate requirement, so that its inclusion does not affect the market for other renewable sources of energy like wind, solar or biomass. In February 2015, India’s first proposed hydro-electricity project to be built on a viability gap funding (VGF) basis and PPP mode appears to have fallen flat as the Mizoram government signs an MoU with the North-East Electric Power Corporation (NEEPCO) to take up the planned project in northern Mizoram. The project 210 MW Tuivai HEP was cleared in 2013 to become the country’s first VGF-based HEP in 2013, meaning the Centre was willing to foot up to Rs 750 crores of the total Rs 1,750 crores the project is estimated to cost. The project was envisaged such that it fell under the state sector, meaning Mizoram would have the rights to use as much of power generated for its needs and sell the remaining as it deems fit. But even then, plans fell through towards the end of last year as banks and private developers shied away from going ahead with the project, leaving the state government to look for other alternatives. The Indian Express. India’s first VGF hydro-power project falls through, Mizoram hands it over to NEEPCO. 11 Feb 2015 <http://indianexpress.com/article/india/india-others/indias-first-vgf-hydro-powerproject-falls-through-mizoram-hands-it-over-to-neepco/>

24) Securities and Exchange Board of India. Memorandum to the Board: Disclosure Requirements for Issuance and Listing Green Bonds. <http://www.sebi.gov.in/sebi_data/meetingfiles/1453349548574-a.pdf>

25) International Hydropower Association Communications Team. What will the Paris Agreement mean for hydropower development? Jan 21 2016. <https://www.hydropower.org/blog/what-will-the-paris-agreement-mean-for-hydropower-development>

26) International Hydropower Association. Hydropower Status Report 2017. <https://www.hydropower.org/2017-hydropower-status-report>

27) The World Bank. Rampur Hydropower Project. <http://projects.worldbank.org/P095114/rampur-hydropower-project?lang=en>

28) External Commercial Borrowing (ECB) Policy – Take-out Finance. Jul 22 2010 <http://allindiantaxes.com/rbicir10-11-4.php>

29) Door to Door tenor/maturity is a term that is mostly used in finance sector. It is generally used to indicate the total period within which the total debt borrowed is to be paid, this total period also includes the period of moratorium (that is the period for which payment has been postponed).

30) Reserve Bank of India. RBI/2011-12/ 9,Master Circular on External Commercial Borrowings and Trade Credits. Jul 01 2011 <https://www.rbi.org.in/scripts/BS_ViewMasCirculardetails.aspx?id=6501>

31) Strategic investors, venture capital, private equity are the principal providers of equity funding to RE projects. Private equity funds have dominated the equity investment scene. Majority of the investments are in INR and the funds stay invested in the companies for a period of 5 to 7 years. Typically, the hurdle rates for direct equity investments range between 16 and 20 %, and are dependent on factors, such as the size of the project, the background of sponsor, the technology risk, the stage of maturity, and geographic and policy risks. On a related note, there have been talks of Mezzannine financing. So, what exactly is meant by this, and has India had an instance of such financing? Mezzanine Finance is a form of quasi debt/equity instrument, wherein sector-specific investors or short-term investors park their funds assuring higher returns (typically 15 % more than the debt instruments). This facilitates availability of low cost equity to project promoters. The investment is secured by charging on assets after assigning first charge to the term-loan lenders. Mezzanine Finance is typically associated with debentures offered to the investor with an option to convert them to equity at a later stage. This form of finance offers flexibility to meet both the investor’s and the company’s requirements, and also provides medium term capital without significant ownership dilution. Mezzanine finance is less risky than equity for investors, as it provides fixed interest along with principal repayment and minimum guaranteed returns to investors. It is normally used in situations where the company is generating adequate cash flows to service coupon payments and the promoters are unwilling to dilute their equity stake in the company. The Indian RE market has seen very few mezzanine finance transactions. Few of the noteworthy transactions are – Mytrah Energy raised USD 78.5 million from IDFC Project Equity and USD 19 million from PTC Financial Services. Solar IPP Azure Power raised USD 13.6 million from Germany’s DEG.

32) Government of India, Income Tax Department. Income Tax Act 1961. <http://www.incometaxindia.gov.in/pages/acts/income-tax-act.aspx>

33) Capital Adequacy Ratio is a measure of bank’s capital, and expressed as a percentage of a bank’s risk weighted credit exposures. Also known as capital-to-risk weighted assets ratio (CRAR), it is used to protect depositors and promote the stability and efficiency of financial systems.

34) Romero, M. J. Where is the public in PPPs? Analysing the World Bank’s support for public-private partnerships. BrettonWoods Project. Sep 29 2014 <http://www.brettonwoodsproject.org/2014/09/public-ppps-analysing-world-banks-support-public-private-partnerships/>

35) Medallo, J. & Sampaio, A. Ongoing Trends in Hydropower. Coalition for Human Rights in Development. <http://rightsindevelopment.org/project/trends-the-rise-of-hydropower/>

36) ibid.

taken from here